On May 15, 1932, there was an attempted coup d’etat in Japan, led by a militant, nationalistic faction in the Imperial Army. The principal victim was the Japanese Prime Minister, Inukai Tsuyoshi. The perpetrators of the coup were given relatively light prison sentences, a pointer to the less democratic and belligerent Japan that would soon follow.

The bizarre element of the coup, which fortunately did not succeed, was a plan to murder the actor Charlie Chaplin. The thinking was that such a deed would incite popular fury in the US, and thus lead to war, in which Japan would prevail. At the time of the coup, Chaplin was watching a sumo wrestling match with the Prime Minister’s son, and thereby escaped the assassins.

This was more than lucky and in many ways Chaplin’s film The Great Dictator is a fine riposte to the destructive nationalism and totalitarianism that took hold across the world from the mid 1930’s. It is a film that still resonates today in our world of ‘predators’.

While our view of Japan today is of a placid, highly civilized country, its history in the past two centuries is a reminder of the pitfalls of isolationism, nationalism and war – concerns that are now echoing louder across the international political economy debate. It should be said at the same time that the post second world war relationship between the US and Japan is a good example of how two feuding countries can come together (Al Alletzhauser’s ‘House of Nomura’ is good on this topic).

Yet, such was Japan’s economic rebound after the second world war that America feared the rise of Japan as it now does China, and fans of economic history may know that during the 1980’s and 1990’s Donald Trump was an eminent Japan-trade basher. For instance, the April 13 1987 cover of Time magazine carried an image of Uncle Sam pitted against a sumo wrestler under the banner ‘Trade Wars – the US gets tough with Japan’ (the stock market crashed five months later).

Now, following decades lost to the after-effects of its economic crisis, Japan is undergoing an awakening, spearheaded by the historic election of the first female prime minister of Japan, Sanae Takaichi. This awakening takes different forms, a more assertive diplomatic stance on China, a ramping up of defence spending amidst greater public comfort with the idea of Japan as a budding military power. Also, Japan’s government is ambitious for its economy and has announced a record state budget of 122 trillion yen (over Eur 600 bn), and Japanese firms like Softbank are in the vanguard of the AI boom.

There are two other financial aspects of this awakening. In an attempt to revitalize the Japanese economy, the Bank of Japan had kept interest rates at or below zero for some time. It has abandoned that policy recently and with both growth and inflation picking up, bond yields have surged. For much of the last fifteen years, the ten-year bond yield in Japan has been well below 1%, but in 2024-25 normalised toward the 1.5-2% range, and is now 2.7%, whilst the longer term 30-year bond yield is 3.95%.

As one of the world’s most indebted countries (Japan’s headline public debt to GDP ratio is well over 200% according to the IMF), the effect of this is that fiscal policy is increasingly smothered by the effect of interest payments on that debt, and policy is trapped between trying to grow the economy, control inflation and not upset the bond market.

Equally the yen is grabbing attention, falling to a forty-year low this week. Indeed, it might well be lower, but traders are wary of a market intervention by the Japanese authorities. There are several factors driving this, the hedging of foreign exchange risk by investors buying Japanese assets, real interest rate differentials, and worries over the effects of expansionary fiscal policy. A costly bout of yen intervention might be close.

As Japan’s asset prices hit records for largely the wrong reasons, it serves as a reminder that many large indebted economies exist on a financial tightrope between growth and calamity. Britain is the most prominent example, but Japan is a more systematic case and over the summer could be the source of a market wobble, if not outright crisis as bond market sell-offs become more common in our ‘age of debt’.

It’s all enough to make me think of Charlie Chaplin’s depression era film Modern Times.

The advent of the Kevin Warsh Federal Reserve with its first meeting last Wednesday, very likely heralds a new departure in American central banking. The Warsh Fed will likely be less effusive in its communication (notably there will be less public defending why the Fed doesn’t hit its forecast levels of rates and inflation), will be more closely coordinated with the Treasury, and if the track record of the new governor is to be believed, will be much more reluctant to use the balance sheet of the central bank to support markets and the animal spirits of the economy. The real test of this will be next economic crisis, potentially a public debt crisis that starts in the next couple of years.

In the medium term, the backdrop to the Warsh Fed will likely be characterised by tighter liquidity conditions. Warsh will likely slow the Fed’s reserve accumulation program, equity issuance by tech firms, IPOs, new bond issuance (again, for AI infrastructure) will also mop up market liquidity and following a bout of bond retirement in the second quarter owing to a bumper tax take, the US Treasury will increase debt issuance from the end of June onwards (up to USD 600bn in Q3).

So broadly speaking from a ‘plumbing’ view of markets, there will be less liquidity shooting around the pipelines of markets. Ordinarily, this is not great news for risky assets like equities, especially with valuations at the very top of 100-year ranges. However, the asset class that intrigues me, is bitcoin, already a significant underperformer this year. The mystery being that bitcoin has yet to reveal its true identity as an asset class, let alone a money.

Bitcoin was established in the aftermath of the global financial crisis, as an alternative to paper money and the institutional framework around that money (i.e. the Fed and the ECB), but has failed in this aim. Bitcoin is not a money. It is simply far too volatile to act as a reliable store of value or basis for payment. Also, the technology associated with cryptocurrencies is also complex enough to dissuade most households from using them.

As a case in point, I can recall that in bitcoin’s early days (2016), train stations in Switzerland’s ‘Crypto Valley’ had a facility to exchange swiss francs for bitcoin, and the canton accepted bitcoin as payment for taxes and services. But transaction fees were very high, and this experiment hasn’t caught on. In fact, only some 0.1% of tax settlements in the canton of Zug were paid in bitcoin.

While the Swiss authorities were happy to give bitcoin the benefit of the doubt, most institutions in the old-finance world, primarily central banks who plan their own digital currencies, have an incentive for it not to succeed, and famously in 2021 Christine Lagarde referred to bitcoin’s ‘funny business’.

Reflecting this, the weakness of bitcoin has not been the technology, but rather the infrastructure around it, and the people who have used it as a means of payment. In the past five years, a good number of exchanges (in Asia) and brokers have collapsed or been shut down, and the entry and exit points to the crypto world are under examination from tax authorities. Also the anthropology and sociology of those who populate the crypto world is crucial to how these assets behave and subsequently to their risk characteristics. In this light the, fact that the biggest holder of bitcoins is apparently the FBI says a lot.

Bitcoin, and the broader crypto world, now face two new competitors of sorts. One is the growth of stablecoins (which are based on the Ethereum blockchain), which may facilitate ‘grey’ economy transactions far more efficiently than bitcoin. The other is AI, whose claim on the electricity and energy sources of the world, makes the production of bitcoin more expensive. Lurking in the future is quantum technology, which some fear could break the bitcoin protocol.

So, bitcoin is far away from meeting the objectives of a ‘money’, and in my view is a ‘tulip’, a speculative, trading asset. It also seems to me that many people are increasingly happy with bitcoin being assigned this role, and much of the interest and eco-system that is developing around it underpins the role of bitcoin as a speculative asset rather than as a bona fide currency.

As such, this points to bitcoin and crypto currencies being ushered into the corner of eclectic trading assets – though less of an experience than horse racing, with none of the aesthetic bonus of art and not quite the fun of collecting wine.

These assets tend, in my experience, to be driven by waves of liquidity, and surges in wealth, as opposed to more fundamental factors. Thus, with the prospect of weaker liquidity ahead, bitcoin is in for a test. It has been claimed that bitcoin is a safe haven, or digital gold, but in general its tendency is to weaken as macro uncertainty rises. It might be the first victim of the Warsh era.

A very early career memory of mine came in late 1999 when the UBS investment bank took the team of analysts covering the staid Paper & Packaging team and re-directed them to become the ‘dot.com’ team. This I reckon came about six months before the peak of the ‘dot.com’ bubble and, I am now wondering if investment banks are channeling resources into AI banking teams (surely AI can do the work!). If so, it would be proof of the idea that AI is everywhere, from the Mythos breakthrough we wrote about a few weeks ago to, with good timing the thoughtful note, Magnifica Humanitas, from Pope Leo XIV on how AI should be deployed.

Nowhere is the sense that AI is everywhere more true than in finance. According to Pitchbook, 45% of all American unicorns (venture-backed companies with a valuation above USD 1bn) are AI-driven, not bad for a technology that, to public eyes, barely existed three years ago. In more detail, two earlier venture-backed successes, Bytedance (i.e. TikTok) and Uber had been established for 80 months when they launched their first products. OpenAI and Anthropic have done so after 30 months, and each is now worth close to USD 1 trn. Equally, illustrating the link between investor exuberance and AI, the FT recently estimated that two-thirds of the value of SpaceX is attributable to investments made in the company in the six months since December 2025.

When this trio of AI firms lists on the stock market, revised index inclusion rules will add their weight to the already substantial 44% representation of technology stocks in the major indices. To that end, AI is no longer a market theme or fad, but is becoming an asset class in its own right.

One of the factors that distinguishes a genuine asset class from a market theme or fad is the presence of a transformative technology, with a lasting economic impact. In the context of an otherwise pedestrian US economy, AI capital expenditure is the dominant growth driver and in the last year, expenditure on data centres in the US hit USD 1 trillion.

A comprehensive study from Stanford’s Forecasting Research Institute (March 2026) compared GDP forecasts from different types of forecasters – economists in the private sector, academics, AI experts and the general public. Unsurprisingly, those closest to the AI industry tended to have the highest GDP forecasts, while academics were more grounded. On balance though, there is a consensus view that AI will lift the trend rate of growth in the US.

There are also increasingly varied ways to invest in AI. An AI-centric portfolio can now span private equity, venture capital, infrastructure (clean energy for data centres), real estate (data centres), currencies such as the Korean won, corporate bonds (Amazon, Meta, Oracle and Alphabet have issued nearly USD 150bn in bonds this year) and private credit. Indeed, AI-related private credit investments are expected to grow by over USD 1.5 trn in the next two years. While there is already a rich mix of AI-centric asset classes, the correlations between them remain high, limiting the diversification benefit.

In addition to investment banks committing resource to AI-driven deals, another hint that AI is an emerging asset class is that it has its own distinctive mode of corporate governance – strong-willed founders who monopolise voting rights, enormous pay packets and neutered boards. This concentration of control is likely to prove one of the structural vulnerabilities of the AI complex as scrutiny from regulators and institutional investors intensifies.

Given the scale of AI’s footprint across markets, one of the essential tasks for investors will be to identify assets uncorrelated with AI (e.g. luxury goods, food), as well as hedges on AI assets. And, as the suspected AI bubble grows in value, investment managers will have to find ways of protecting portfolios against sharp reversals in AI valuations.

The investment dimension of the AI boom carries particular urgency. Given the risk that AI (as per Mythos) creates potentially existential security and economic risks, and could disrupt labour markets, there is a strategic need for pension funds and sovereign wealth funds to have exposure to the economic benefits of AI. As it stands, the risk is that billions of people will have their lives and livelihoods changed by AI, but the benefits accrue to only a narrow group of investors and executives. In that regard, the advent of AI as an asset class gives individuals, countries and investment funds a means of participating in the upside of the AI boom.

The one formidable obstacle investors will have to navigate is the sense that we are in the thick of an AI bubble. Already long-run valuation measures – such as the ratio of market price to long-run earnings (the ‘Shiller P/E’), or the ratio of the value of the US stock market to GDP – are testing all-time highs, at levels not seen since 1929 and 2000. In this way, AI is truly everywhere, in our savings, investments and pensions, and that will be a risk.

To return to my first point on the switching of analyst roles. A couple of brokerages have, according to the Wall Street Journal’s China correspondent, dropped coverage of Chinese consumer stocks because of the weak outlook for spending. It might be the next trend to watch.

As a child I was fascinated and terrified by tales of the Bermuda Triangle, an area between Florida, Puerto Rico and Bermuda where ships and planes disappeared without warning, allegedly. Legend had it that a mysterious magnetic field around the Sargasso Sea drew vessels to perdition, or that even darker forces were behind the disappearance of the crew of the Mary Celeste.

Without stretching the analogy too far, my feeling is that financial markets have entered a logical Bermuda Triangle, or even Trilemma. Data, models, rules and indicators go in, but come out logically impaired. In particular, there is an unreal sense from at least three asset classes that are at historically extreme levels, each apparently contradicting the other. They cannot all be right.

In one corner, the US has, for the first time since 2007, issued long-term debt (30 years maturity) at a yield of 5%. Then, US stock market valuations are at an all-time high since 1929 and, as we stressed in last week’s note, semiconductor stocks are in a speculative frenzy. In another corner of the triangle, oil prices are pushing the highs of the last two decades.

This trio of market signals leaves investing logic in a grey zone — a Bermuda Triangle-like make-believe world. This stretched logic suggests that the prosperity and productivity of AI-related capital expenditure will rescue the world from both high inflation and a debt crisis, and will also prove powerful enough to compensate for the effects of a momentary energy crisis. I am not sure.

The confluence of these three indicators is interesting because each one points to a long-term trend that investors and policymakers cannot ignore, but equally, each one rests on a short-run vulnerability.

Rising bond yields in Europe, the UK, Japan and the US are an early warning of a debt crisis, or debt purgatory, to come. In the very short term, they signal that inflation is creeping higher whilst a number of policymakers — notably on the Fed’s FOMC — appear complacent about this development.

Equities are trading at record high levels and valuations, mostly because earnings and business cycles are strong. But a very small number of stocks has pushed the market higher, caused in part by the fact that sectors like semiconductors are heavily financialised. What I mean by this is that the deployment of exchange-traded funds and options has surcharged the prices of semiconductor stocks, and likely driven them well above long-term fundamental valuations.

In my view, Intel’s ability to treble in value since the end of March (from USD 41 to USD 129 last week) has less to do with the fundamentals of the company, and more to do with speculation. In support of this, a recent Goldman Sachs note shows that retail investors now account for around 20% of US stock market trading.

Energy prices remind us that in a multipolar world, commodities — or rather their supply and refinement — acquire a premium, and that a number of countries will have to address shortcomings in industrial supply chains. For example, last week Willie Walsh, the former airline chief executive, warned that the UK has scant jet fuel refining capacity. As such, energy infrastructure will be an area for future investment.

In the short term, however, supply pressure may be more acute: oil inventories are being drawn sharply lower. Unless there is a full and speedy resolution to the Iran War, estimates from JP Morgan point to world oil inventories dropping to 6.8 billion barrels by September — just enough to keep refineries operating worldwide.

So, like the Sargasso Sea, market compasses are spinning in different directions, and it is difficult to discern a clear narrative. The confusion arises from the changing geopolitical nature of the world, the fast shift in industrial structure away from ‘bits’ and towards ‘atoms’, shortages of refined oil and compute, and the intense financialisation of specialised sub-industries such as semiconductors and commodities.

Given the disagreement between markets, the obvious question is: which one is right? A ‘two-handed’ economist might argue that the stock, commodity and bond markets are all correct, but on different time frames.

In my experience, the bond market is the most consequential, because when it worries, it imposes a cost on other markets and on political actors. The overused but apt quote from President Clinton’s adviser James Carville in the mid-1990s captures it well: “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

So, the ‘market triangle’ or trilemma is resolved by bonds showing their displeasure at high oil and inflation, slowing the economy and walloping the over-bought sections of the stock market.

From a policy angle, bond markets are highlighting the urgent need for policymakers to calm inflation — through rate rises from central banks, and an early test for incoming Fed Chair Kevin Warsh — for governments to reduce debt, and for greater policy clarity in countries like the UK. The silver lining is that credit markets are so far well behaved, signalling that the healthy business cycle should allow for these policy actions to be made now, before it is too late.

A long time ago, when I completed my postgraduate studies, I shelved my thesis (on the relationship between corporate governance and company performance) away in a dusty library, thinking that, like many academic works, it would have no relevance in the world of business. Yet, soon after, as the tide went out on the dot.com bubble, a series of major corporate governance scandals surfaced (Enron being the most prominent).

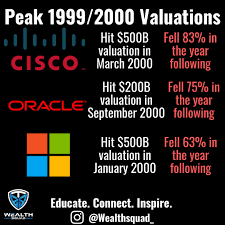

Hopefully my sense of timing is better with experience, and I have started to think of the corporate governance/performance link again. There are a few recent triggers. The value of Intel, having languished in the doldrums for decades, has recovered toward the levels seen in 2000. Taiwan and South Korea, as we noted last week, have become two of the largest stock markets in the world. A range of valuation measures for the US market and indicators of retail participation in the market, are at 2000 nosebleed levels. It also seems that technology companies are growing on steroids, Samsung has become a USD 1 trillion firm last week and Nvidia is now worth USD 5 trillion.

The really new development is the advent of mega-cap startups like Anthropic and SpaceX, both of which have raised capital at valuations close to USD 1 trillion. Trotting behind them, according to the May edition of the Pitchbook Unicorn Tracker (a unicorn is a private company with a value of USD 1bn or greater), are 1,680 unicorns. There were 44 when the term was coined in 2013. Today’s unicorns are worth close to USD 9 trillion (the top 3 companies are worth USD 2.5 trn). About 40% of the total unicorn value is made up of AI firms, which suggests that they are very young indeed. In the history of economics and business, this is an entirely new phenomenon. For it to have happened, several things have changed since the dot.com bubble.

The first is that public and private markets have grown impressively. Not only are US public markets the largest that they have been relative to GDP, but private capital (private equity, venture capital, etc.) is now becoming a sizeable source of financing internationally. As it does, different forms of investor are emerging within it – private credit is the one that currently gets attention, but many growth capital investors have helped to push unicorn valuations to extremes for fear of missing out on hot deals. For example, the median value of late-stage venture deals in AI firms is now USD 5bn, a USD 4bn premium on non-AI firms.

An interesting new element in capital structure is that new, fast growing firms count governments as shareholders, as well as the ranks of former officials and those in the political ecosystem (France’s Mistral is a case in point). Further, the large technology firms have also become active venture investors, and in many recent earnings reports the item ‘other income’ popped up, showing how the likes of Microsoft are already reaping the benefits of their investments.

Two other significant changes are worth flagging. The advent of social media and, more recently, AI-driven commerce means that successful companies can grow very quickly. Large established firms like Apple, Microsoft and JP Morgan have taken decades to grow but are being ‘caught’ by young companies with relatively small workforces, and the effect is disruptive — largely, though not always, positively so. This is much less the case in Europe, which also lacks the small but critical cohort of individuals who know how to build and scale new firms rapidly.

The emergence of a new business model is well-timed for the evolving world order. Recall that the Joint Stock Company Act of 1844 helped to spur the expansion of the British empire in the 19th century, the arrival of the ‘global business model’ (Theodore Levitt’s 1983 essay ‘The Globalization of Markets’ captured this development) was the modus operandi through which America transmitted globalisation around the world (or as one economist put it multinationals were the ‘B-52’s of globalization’).

However, to my original statement, the arrival of new, fast-growing, private companies (many of which are pre-IPO firms), comes at a time when corporate governance in the US is at a low ebb, in terms of the alignment of executive pay with outcomes, active boards, shareholder vigilance, and oversight by institutions like the SEC and Department of Justice.

Further, new, young companies bring their own governance foibles. Many are led by individuals with strong personalities, a necessary quality in startups, many would argue, but an undesirable one from a governance point of view, especially where technologies like AI demand ethical guardrails in their deployment.

Further, many fast growingfirms have complicated capital structures and voting rights. In the past, slower-moving capital market cycles and better regulation might have weeded these out, but have instead become the norm. Incorporation in regulatory ‘paradises’ (more businesses are set up in Texas for instance), the prohibition of shareholder class actions, non-profit structures and heavy share-based compensation have become the norm. This matters because more retail investors can access ‘soon to be private’ companies, in addition to subscribing for IPO’s.

Above all, many of these firms have as yet little to show in terms of profits and in the context of stratospheric valuations, the risk of a bubble is high. Once the AI capital expenditure boom slows, the tide will go out —as Warren Buffett famously observed, and many will lose their capital, and will wonder if they should have paid more attention to corporate governance. If they do, I have an old study to share with them.

One implication of the recent surge in the price of semiconductor firms is that the stock markets of Taiwan and South Korea are now larger than that of the UK (which in 1900 made up 25% of the world stock market capitalization). It is expected that the two East Asian countries will soon have more billionaires than Britain, many of whom have apparently been scattered to the winds by the Labour government.

Though a country’s stock market is a highly imperfect indicator of a country’s economic standing, it does offer good clues as to evolving industrial structure. Bond yield and currencies help to complete the picture, and the runaway UK 10-year Gilt yield (now above 5%) doesn’t tell a happy story either. Then, on GDP, the country whose rise impresses me is Poland, which has not suffered a recession in the past thirty years (COVID excepted). Its GDP has increased sevenfold since 1990, and by 2030 it is expected to surpass the UK in terms of GDP (based on purchasing power parity). Remarkably, Poland is also shaping up to be a geopolitical power as well.

The loosening of the globalized world order, and the advent of many new risks and challenges – from the impact of AI on economies, to climate damage to war – has the potential to knock some nations back, and present opportunities to others.

As such, we can expect that the rise and fall of stock markets and economies tells us a lot about the rise and fall of nation states. In a world where the established world order is shattered (OPEC is the latest long running institution to fall apart), the rise and fall of countries is accelerating, and has become more vivid. In 2020, in the context of how different countries and states were responding to the COVID crisis, we wrote of the idea of the ‘League of Nations’, and have emphasized the theme ever since.

There are many existing league tables of country performance – happiest nation, most innovative country and most competitive, to name a few. Those league tables tend to be dominated by small, advanced economies. Regular readers will know that one of my favourite long run economic themes is the success of the small, advanced economy model, notably so for the way in which these nations can adapt to changes in the broader world. The UAE is a case in point.

In previous notes I have also made the parallel between football and politics, and this is still valid. A few weeks ago I mentioned that in the last ten years the UK has had more ministers for housing (a whopping 14) than Chelsea FC has had managers (12). Chelsea have recently parted with their latest manager Liam Rosenior, and it might well be that a cabinet reshuffle or change of prime minister leads to Matthew Pennycook moving on from his job as UK housing minister.

Like football, the manager of a country is important. For decades, Singapore and the Emirati states have made a virtue of strong, visionary leadership, Greece’s Kyriakos Mitsotakis and more recently Mark Carney in Canada are associated with turning their nations away from troubled waters.

In today’s League of Nations, the winning formula is changing, and shifting towards all things ‘sovereign’ and ‘atom-like’. For example, last week Canada announced the creation of a sovereign wealth fund to help the buildout of critical infrastructure, and it also laid claim to be the host of the new multilateral defence bank (Chris Collins and I wrote about this in a recent note for Barrons). Further, as I mentioned last week’s note (‘Mythical’), successful countries will need to cultivate their own AI stack, and the merger of Cohere and Aleph Alpha is a sign of things to come (their main shareholder is German but the firm will effectively be Canadian from now).

Then, with a step change in the industrial structure of the developed economies of the world underway, from services and ‘bits’ (software, crypto) to ‘atoms’ (energy, infrastructure, defence, AI and quantum), those countries with the universities, capital base and innovation ecosystems, will thrive. America is the standout example, but the Nordic countries and the economic zones that surround the Alps (particularly Switzerland) are good examples.

One consideration regarding the stature of nations is age and pedigree. One of the elements that makes small, advanced countries successful is that their laws, democracies and institutions have been in place for some time, and therefore offer clarity and consistency to businesses for example. At the same time, as economies get older they can become sclerotic, acquire layers of regulation and fail to engage in the creative destruction necessary to keep economic growth at healthy levels. Whilst this is simply an observation, I have a hunch that like aging athletes, older, large economies (US, Japan, UK, France) resort to a ‘boost’ in order to keep their economies going, which may explain why they are excessively indebted.

A final word in praise of older economies and societies, which relates to the cultures, behaviours and ‘family silver’ they accumulate over time. King Charles III’s various speeches in Washington last week demonstrated the value of heritage, and he might just have saved Britain from relegation to the lower leagues.

One of the characteristics of a chaotic world order, that is on one hand bedazzled by a new technology and on the other, deeply troubled by multiple wars and economic stress, is the disagreement of different markets about the state of the world. For example, the US stock market has recently hit new highs, but at the same time, many parts of the commodity complex portend an energy crisis (in Asia and Europe mostly) and a food crisis (in Asia and Africa).

Often these disagreements occur when sets of investors are laser focused on very specific asset classes, and perhaps do not talk to each other as much as they should. For a long time, this was a perennial problem between the equity and credit departments of investment banks. In periods of stress, credit analysts often had a much more negative view on individual companies than their equity analyst counterparts. I recall that during market crises (dot.com and global financial crisis), some banks brought credit and equity analysts together, so that the balance sheet and profit and loss statement could speak to each other, as it were.

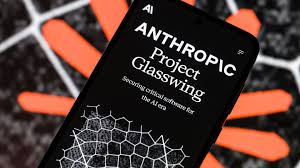

This initiative came to mind last week when I read that in one part of the impressive, new JPMorgan headquarters in Manhattan market strategists were busy upgrading the bank’s 2026 forecast for the S&P 500 index to 7600 while very likely in another part of the JPMorgan building, lawyers, bankers, chief technology officers are scrambling to figure out the implications of Anthropic’s latest model Mythos for the banking system. Many of you will have read that upon the launch of the model, the Treasury Secretary summoned executives from the largest American banks to ponder how Mythos, if used the wrong way, could collapse the financial system.

Mythos is impressive, but also very scary to put it simply. In tests it has easily outperformed other Anthropic models and outperformed to the very upper limit of cybersecurity related tsests, detecting thousands of cyber vulnerabilities in software it tested. The problem is that the unconstrained Mythos can do the exact opposite, exploit bugs in software, and execute deadly attacks on IT systems.

Because of this Anthropic has limited the release of Mythos to twelve companies (‘Project Glasswing’), and the aim of this initiative is to find and repair deficiencies in software. The risk of course is that other platforms or states manage to develop models as powerful as Mythos (some Chinese models are said to be only seven months behind) and apply these to nefarious ends. Indeed, there are reports that three major Chinese AI firms have set up 24,000 accounts on Claude in order to try to hijack its capabilities.

The fact that the Treasury, and other bodies like the Bank of England, are scurrying to determine Mythos’ threat to financial systems is of great concern, and the advance of this model is now a national security issue across most developed nations. The risk of a large, near-autonomous attack on software infrastructure, financial systems and public institutions is now very real, and makes Robert Harris’ 2011 book ‘The Fear Index’ highly prescient (it’s one for the beach this summer).

The advent of Mythos also strikes a chord with a chart in a recent research paper from the Dallas Federal Reserve that illustrates the potential for AI to affect long-term economic growth. Economists normally deploy three types of forecasts – a baseline that tracks historic growth rates, an optimistic version a little above it, and a corresponding pessimistic one. In this paper, however, the optimistic scenario goes vertically upwards and the pessimistic one goes vertically downwards, capturing the potential of AI either to revolutionise the economy or to destroy humanity. In a later chapter I explore the economic and financial effects of AI in more depth, and how it may trigger or exacerbate a debt crisis.

More importantly, it brings into focus the idea of sovereign AI, the idea that governments control and need to control AI models and their data, energy and funding supply chains. Anthropic’s recent popularity is partly based on its independence from the US administration, but it is nonetheless in the American camp. China is catching up fast (DeepSeek is taking on new investors) but, apart from Mistral, Europe is lagging.

There are several things’ governments can and must do, and I am thinking of democracies like the UK, Japan, Canada and the EU. The first is state capitalism (a full description of which is outlined in a recent note from David Skilling), and this can involve sovereign wealth funds taking bigger stakes in AI model builders, the build out and reform of energy systems, and the further concentration of poles of AI excellence. Europe has been too slow here so far, and in my experience confuses the initiative towards state capitalism with a disinterest in incentivising private investment.

A further initiative will be the enhancement of national cyber security institutes in the context of greater collaboration between aligned nations and a rethinking of how critical infrastructure works, is powered and where its multiple vulnerabilities lie. The terrifying risk is that AI is developing so quickly that a small group of malicious individuals, aided by a small army of cyberagents, could disable a small country like Belgium.

When ChatGPT came to light in 2023, the key figures in the industry issued two letters (‘The Pause Letter’ in March 2023, and ‘The Extinction Letter’ in May 2023) that warned of the capabilities of AI and of its potential misuse. The letters were greeted with some scepticism, and in the giddy rush of AI stocks were quickly forgotten. It turns out that the founders may have been on to something.

An unusual but non surprising cameo in the response of the UK to the burgeoning energy crisis that is resulting from the Iran War, was the inclusion of Bank of England Governor Andrew Bailey in last Tuesday’s emergency COBRA (Cabinet Office Briefing Room) meeting. The prospect that inflation and a cost-of-living crisis could further derail the fledgling economic recovery in the UK, has struck fear into politicians (the OECD reckons that the UK will be the worst hit country), though monetary policy purists won’t like the appearance that the independence of the ‘Old Lady’ (the Bank not Bailey!) is compromised.

What is more interesting is that this is yet another datapoint in a trend where finance, war and politics are becoming interwoven. In peacetime, central banks were the only game in town, the monetary battleships of the 2010’s, keeping the peace in bond markets and tilting currency moves in their country’s favour.

That was not always the case, books like Liaquat Ahmed’s excellent ‘Lords of Finance’, show the key role that central banks played in maintaining the stability of war time economies.

Now, the world order that is unravelling before our eyes is more like that of the 1910’s than the 2010’s, and a particular concern for central bankers is the extent to which economies have become frictioned.

By this, I mean the extra costs and inefficiencies that are bubbling up because of the end of globalization (a period associated with intense commoditization of prices and low inflation), a pandemic of supply chain disruption, and great power competition for ‘rare’ things (from rare earths to rare places like Greenland to rare technologies like quantum computing).

In general, these frictions will tend to bump up the rate of inflation. A famous example is the way in which the side effects of the war on Ukraine combined with short-sighted energy policy in Europe to produce a prolonged rise in inflation from 2021 to 2022.

From the point of view of central bankers, inured to a decade of stubbornly low inflation, this was a surprise, and prominent members of the central banking community were badly caught out by their view that this burst of inflation was ‘transitory’. Their difficulty is that the economic context of the 2010’s was characterised by demand weakness whereas the main policy problem of the 2020’s is supply constraint.

We now live in an economy of ‘atoms’ (energy, commodities, deeptech), where historically huge amounts of investment capital expenditure is/are being deployed amidst supply constraints to build a new (AI) economic infrastructure. About half of this will be financed by different forms of credit. Within this model, the debate on the productivity benefits of AI, which has produced a wide range of estimates of the potential impact of AI on the economy, illustrates what a demanding environment it is for central bankers to read.

The potential energy shock from the Iran war complicates matters even more and raises the prospect of a policy error. Echoing the schoolboy mistake by Jean-Claude Trichet to raise interest rates in 2006 when a spike in the dollar helped trigger a spike in oil prices, current ECB President Christine Lagarde has stated that the ECB was ‘ready to raise rates’. This may be a pre-emptive move to push markets to do the ECB’s job, and to warn companies and unions off raising prices. If not, Lagarde and other central bankers should do no harm. A rate rise from the ECB will do nothing to re-open the Strait of Hormuz (good note on the disruptive effects from the Kiel Institute), nor to rebuild refining capacity in the Gulf states.

The dilemma for central bankers is in distinguishing between an energy centric rise in prices and an eventual generalised rise in inflation expectations.

In my view the economic consequences of the Iran War can be short lived, but as long as it endures, amounts to a tax on consumers, a hit to risk appetite and a blow to confidence in US financial assets. Furthermore, the many costs of the war (see our note of two weeks ago, ‘It will be over by Christmas’) include a rise in the debt burden that countries like the US and UK will suffer, and an elevated level of uncertainty as the world’s former policeman turns bully.

It could be worse for central bankers, they could be politicians, who now must contend with another cost-of-living crisis, with little money left in the fiscal jar.

A recent book, Samuel Moyn’s ‘Gerontocracy in America, highlights the growing concentration of wealth and power in the much older generations in the US, whilst younger generations face historically high valuations in real estate and financial assets, and how this growing intergenerational divide might be mended. Moyn, in my view, has struck a chord that will become one of the new dividing lines in politics, in Asia and the West.

His book brings demographic change into focus, a slow-creeping risk to economies, society and public life, but whose implications are only just surfacing in the public debate. Despite that, from a popular point of view, the sense in many Western countries is that there are too many people, or rather that infrastructure has not kept up pace with population growth – I am writing this in Dublin, which is an excellent case in point.

Yet, the long-run demographic trends – falling fertility, longer life expectancy and a shift in population composition towards a much smaller working (tax paying) population, will have enormous impacts on society, pension systems and debt loads, to name a few economic issues.

As much was evident in Germany’s recent pension reform debate which was nearly upended by Helmut Kohl’s grandson Johannes Volkmann and a group of other young parliamentarians who voiced the right of the younger generation to not have to shoulder the financial burden of their parents’ generation (under the German system, and many others, the working population effectively funds the retirement system of the older generation)..

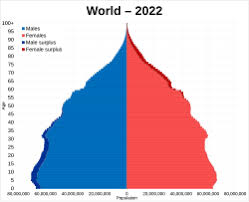

The best starting point on the outlook for demographics is the United Nations World Population Prospects website. and the data – especially in chart form – are quite striking.

The UN data show that as we approach 2100 the world population will plateau and start to shrink. From roughly 2080 onwards the world population growth rate will turn negative for the first time in centuries (wars apart), as the death rate passes out the birth rate. Within the age cohorts, the over 65 group will expand by a billion people in the next thirty years.

More specifically, at the country level, the US death rate will surpass the birth rate in around 2040, and population growth is likely to only be sustained by immigration. The picture is worse for some European countries – Italy for example is already in negative population growth territory, and the most negative forecast scenario from the UN has the Italian population dropping from over 60 million today to 25 million by 2100 (the same level as when Garibaldi unified the country).

Equally, China, which has been renowned for its economic and population growth, will endure a collapse in the 24–65-year age group, who today number 830 million people and by 2100 are expected to comprise 280 million people. China is projected to be the country most affected by ageing, with its, China’s elderly dependency ratio is projected to surpass 100% by 2080, meaning there will be more people aged over 65 than those aged 15 to 65.

The expected collapse in the working population begs serious questions for the economy – who will pay taxes, sustain pension systems and where will demand for financial assets come from. Markets are not worried, yet.

In general, researchers find that there is a positive link between demographics and asset prices, a finding that is predicated on the rise of the boomer middle class and the coincident equity bull market and fall in bond yields. The idea is that until they retire, working households invest more in real estate, equities and other riskier assets, but then shift to income-oriented assets like bonds as they get older and require income from investments. The oddity in that respect is that despite an ageing population, equities and real estate are very expensive. This may well owe to a growing investment culture, a record level of wealth (USD 500 trillion worldwide) and the prosperity boon that has resulted from globalization.

In this context, old money will become a political target, both in terms of demands for lower inheritance taxes, to more populist measures to tax the ‘old’ and give the ‘young’. For governments who worry about demand for their bonds, wealthier older citizens might make ideal candidates for financial repression (their children would face lower inheritance tax provided that capital spent a period of ‘purgatory’ invested in government bonds – I outlined a similar theme in ‘Patriotic Capital’)

At the same time, pension systems will have to change to accommodate a proportionately smaller number of workers (to pensioners). Private pension systems will become more common, they will invest more, earlier, with a tilt to riskier assets.

Concurrently, I expect to hear more on the need for states to establish sovereign wealth like funds (based potentially on the sale of state assets) to help provide for future pension liabilities. Another concern will be the need for states to cushion the potential blow of AI on workforces (a fund that holds equity in AI firms might be an avenue), at least through a transition period. In the long term, AI and robotics may well allow more older people to work for longer and for more women to enter the workforce. And, I haven’t managed to tackle the topic of later retirement ages and how that will impact the workforce and society.

The effects of demographics are not yet showing up in markets, and are just creeping into the investment industry, but it will become a major fiscal and financial megatrend.

It’s that time of year when investors and economists release their prognostics for the year ahead, and eclectic and contrarian as we like to be, The Levelling brings you its top ten themes for 2026, with apologies for the length of the note – in fact this week we are simply giving you the first five themes, with the others to follow next week. It’s really one to print out and read with a coffee, or even a stiff drink.

Given the approach of the holidays, we have also added in some pertinent film and book recommendations.

Some of the ten themes we flag here are based on observations we have made during the year, and relate to trends that are now becoming clearer, chief amongst them is the imprint of AI on economies, geopolitics, and society.

We hesitate to make outright forecasts for GDP and rates for two reasons – first we expect growth to rise modestly during the year (though this is very much dependent on the capex cycle) and second, most of the interesting developments will take place at the sector level.

#1 RAIlway Boom

In the late 1990’s as the dot.com bubble built, there was a polite debate amongst central bankers as to whether or not an asset price bubble was present in stock markets, most notably in dot.com related companies. The upshot of the debate was that even if the central bank could identify a bubble, there wasn’t much it could do to puncture the bubble (notwithstanding Alan Greenspan’s ‘irrational exuberance’ moment).

Today, central banking has changed, and so too have asset bubbles. There is a very broad narrative – from investors and economists – that we are indeed in a ‘bubble’, the only question is whether markets are in the foothills or the peak of the bubble. My sense is more ‘foothills’ than peak, largely because we are not yet seeing the folly and exuberant behaviour that was present in 2000 (I will share some stories in a future note).

Of course, the obvious danger of such a narrative is that for some but not all investors, it permits the belief that investors can continue to buy very expensive assets and later hand them off to ‘greater fools’, and the illusion that ultimately they are not the fools.

Every asset bubble needs an underlying logic, a belief that ‘this time its different’ and this is supplied in spades by the adoption and investment in Artificial Intelligence (AI). Signs that companies and households are deploying AI are manifold. This bubble is also different in the case that AI is producing revenues, as evidenced in the operating and market performance of large AI centric firms (the so called ‘Magnificent Seven’ companies who together now make up nearly 40% of the US stock market capitalization), but those earnings are predicated on the success of the AI business model and are increasingly circular, in that investment by META becomes revenue for Nvidia and so on.

What is altogether less clear to me is how the economics of AI play out. While the adoption of AI is occurring more quickly than other technologies (the internet), competition will surely lower margins quickly. Chinese projects are a case in point, and some of the large US AI platforms, of which OpenAI is the leader, may find their economic models undercut.

Neither is the distribution of the productivity benefits that convincing – specialized firms and operators with access to proprietary data will be able to leverage AI to great benefit, along the lines of my ‘One Man and his Dog’ thesis. However, for most people, once some basic administrative tasks have been swallowed by AI applications, the positive economic impact on their lives might be more limited. Another consideration is that AI model technology is in the hands of a small number of investors, so the capital productivity benefits of it can also be limited.

The Future:The AI boom or bubble is gathering momentum. Levels of capital investment (relative to GDP) are already surpassing those of prior bubbles, but have not yet attained the giddy heights reached during the railway bubble of the 1900’s. The railway bubble was one of the great asset bubbles – and helped build the crucial infrastructure of the first wave of globalization. In 1900, investment in railway infrastructure amounted to 6% of GDP, AI today is just over 1.3%. Also, at the turn of the 19th century nearly 60% of the market capitalization of the US stock market was made up of railway stocks (today it is 0.3%) which as a rule of thumb suggests we might see talk of a USD 10 trn valuation for Nvidia and SPX 10,000 ((the US S&P500 index hitting 10,000 points) as a ‘sell everything’ moment.

Read:Charles Kindleberger’s ‘Mania’s, Panics and Crashes’

#2 ‘Dalloway’

One of the more memorable films I saw in 2025 is Dalloway, a French film starring the ever-excellent Cecile de France, which I hope will make its way to the Anglophone world. The object of the film is to show how pervasive and sometimes pernicious AI could become as a social force, and as we head into 2026, this is a theme that will become more important – in healthcare, labour markets and society – and more startlingly obvious.

To start with an alarming example, in 2021 the Swiss government’s Spiez Laboratory, one of whose specialisations is the study of deadly toxins and infectious diseases, is located right in the heart of Switzerland, performed an experiment where they deployed their artificial intelligence driven drug discovery platform called MegaSyn to investigate how it might perform if it were untethered from its usual parameters.

Like many AI platforms MegaSyn relies on a large database (in this case public databases of molecular structures and related bioactivity data) which it ordinarily uses to learn how to fasten together new molecular combinations to accelerate drug discovery. The rationale is that MegaSyn can avoid toxicity. In the Spiez experiment MegaSyn was left unconstrained by the need to produce good outcomes, and having run overnight, produced nearly 40,000 designs of potentially lethal bioweapon standard combinations (some as deadly as VX). It is an excellent example of machines, unconstrained by morality, producing very negative outcomes. It’s a chilling tale of the tail risks of AI.

More commonly, AI will increasingly become part of our economic and social lives, and its effects will be more apparent.

In labour markets, there is already plenty of evidence to suggest that AI is curtailing hiring, markedly so in the case of graduates. When AI and robotics start to combine, they can have very positive outcomes (in education and elderly care) but in warfare (see the Netflix documentary ‘Unknown Killer Robots’), fruit picking, warehouse management and even construction – to give a few examples, the blue collar labour force will feel the effect. This could set up a political reaction, and we might well see a Truth Social post from the White House to the effect that AI is not such a great idea and needs to be regulated.

A potential side-effect of the more negative effects of AI on the labour market could be a rise in anxiety and what social scientists call ‘anomie’. Much the same is becoming clear from the ways in which social media is skewing the sociability of humans (think of declining fertility rates, pub closures and the mental health effects of social media). As such, the social effects of AI may lead to ‘deaths of despair’. If this is grim, there is potentially very positive news in the use of AI to improve medical diagnoses in inexpensive ways, and the marginal impact of this in emerging countries can potentially be very significant (leading AI firm Anthropic is targeting science and healthcare in terms of applied AI solutions).

The Future:The economic and social side-effects of AI will become clearer – many of them will be positive, but others will start to provoke a political reaction. While the EU has softened some of the restrictions in the EU AI Act, the interesting development is that at the state level in the US there is a growing desire to curb some of the effects of AI, a trend that is supported by case law. Moreover, local politicians in the US (Republican Josh Hawley is an example) are more vocal about the negative side-effects of AI on labour markets and education.

Read:Carl Benedikt Frey ‘The technology Trap’(2019), and Robert Harris’ ‘The Fear Index’ (2011)

Watch: ‘Dalloway’ (1997)

#3 AI Cold War

A further facet of AI to keep an eye on is geopolitics, and as we leave 2025 behind, we will hear more about the notion of an AI Cold War or ‘Sovereign AI’ according to a good Pitchbook note. This emerging idea refers to the strategic uses of AI, in the context of strategic competition between the ‘great’ powers. This race is already on, and the US is in the lead, with China chasing behind (my recent note on The Plenum details how China is prioritizing frontier technologies as the spearhead of its economic plan). Europe is very much in third place, with energy policy and half formed capital markets the biggest obstacle.

In a ‘Cold War’ AI world, model development and deployment increasingly take a multipolar form (see #8 below), regulation is competitive and technology firms closely align with governments – forming symbiotic parts of national infrastructure – while national security considerations are embedded into investment processes and supply chain planning. In time, governments may steer model developers towards new datasets if there is a strategic advantage to be gained.

The Future:From an investment point of view, we expect private equity/credit to become an enabler of this trend, and for their part governments will open up the flow of pension capital to private asset classes. Governments may also become more active investors – either in steering merger and consolidation activity, or in the fashion of the Trump administration, taking stakes in firms that are judged to be strategic. Military uses of AI will become more commonplace, and we will slowly learn more about the effects of this on navigation systems, genetics, finance and social media, to name a few.

Read: ‘Breakneck’, by Dan Wang (2025), ‘Chip Wars’ by Chris Miller (2022)

Watch: Dr Strangelove (1964)

#4 Expensives to Defensives

An age-old joke goes that when asking for directions, the traveller is told ‘I wouldn’t start from here’. It is much the same for investors looking into 2026, though less so tactical traders who believe that they can time the ebbs and flows of the emerging stock market bubble.

The dilemma for asset allocators is that with the US stock market making up some 60% plus (depending on the benchmark) of world market capitalization, and trading at near record valuation multiples (price to earnings or price to long term earnings (Shiller PE), or even market capitalization to GDP (Buffet Indicator), the exposure to American assets is increasingly expensive and risky.

For example, a model that combines monetary, business cycle and market valuation indicators, suggests that from this point onwards, returns in the next couple of years for US equities will be close to zero. Add to that the fact that the dollar still looks expensive and corporate bond (and high yield) spreads are very narrow, and the conundrum for allocators next year will be considerable.

As we end the year, volumes have been very low and speculative activity (options) very high, and this points to high levels of volatility through 2026, and remarkably, a few of the large bank CEOs have warned of significant market drawdowns.

The Future:We expect to see investors put more money to work in cheaper defensive sectors – Staples and Healthcare for example, and for capital to flow to other regions beyond the US. In addition, in the next five years, if multiple surveys of family offices and pensions are to be taken at face value, we expect private assets to make up a much more significant proportion of investment portfolios.

Read: Benjamin Graham ‘The intelligent Investor’ (1949)

Watch: ‘Margin Call’(2011), ‘The Big Short’(2015)

#5 K Shaped economy

In the context of a political-economic climate in the US where good, regular economic data is hard to come by, commentary from industry leaders as they report earnings is providing some fascinating insights. For example, some weeks ago, Chipotle, the burrito chain, reported a surprise drop in revenues because two key consumer groups, households earning USD 100k or less, and younger customers (24-35 years old) are cutting back discretionary spending, even on fast food.

A range of firms with similar client bases underline this trend – car manufacturers report that sales of expensive, large vehicles are strong, but that lower income customers are preferring smaller, fuel-efficient models. McDonalds is revising its ‘extra value meal’ option, and credit card providers like Amex report very different types of activity from rising card balances and distress in the lower segments, to robust spending in its ‘Platinum’ category.

Economists are blithely referring to this phenomenon as the ‘K-shaped’ economy, whistling past the graveyard of economic history that portends revolutions are made of such obvious divergences in fortune.

Now all of the talk is of a K shaped economy – which refers to multiple divergences between the price insensitive wealthy and those in economic precarity who are sensitive to inflation, a services sector that is either shedding jobs and holding back from hiring compared to the upper echelons of the technology and finance industries where unprecedented levels of wealth are being created.

There are two other effects ongoing. The first is the economic effect of AI-focused capital expenditure (across the energy, logistics and technology sectors). The second, more important trend is a mangling of business cycles, such that few of them are synchronized across geographies, or between the real and financial economies (German chemicals is in the doldrums but German finance is on an upswing).

Yet, a better diagnosis might be the ‘Marxist’ economy – one where the owners of capital and the source of labour are at odds.

The Future:In the US, the top 10% of the population own 87% of stocks and 84% of private businesses, according to data from the Federal Reserve. On the other hand, we have previously written about the rise of economic precarity in The Road to Serfdom. So, whilst it is a new observation amongst the commentariat, the diverging fortunes of capital and labour should start to trouble policymakers in 2026. Expect this to be a headline policy issue net year – the White House is already paring back some tariffs, and in Europe governments compete to either tax the wealthy (France and the UK) or to lure them (Italy).