A very early career memory of mine came in late 1999 when the UBS investment bank took the team of analysts covering the staid Paper & Packaging team and re-directed them to become the ‘dot.com’ team. This I reckon came about six months before the peak of the ‘dot.com’ bubble and, I am now wondering if investment banks are channeling resources into AI banking teams (surely AI can do the work!). If so, it would be proof of the idea that AI is everywhere, from the Mythos breakthrough we wrote about a few weeks ago to, with good timing the thoughtful note, Magnifica Humanitas, from Pope Leo XIV on how AI should be deployed.

Nowhere is the sense that AI is everywhere more true than in finance. According to Pitchbook, 45% of all American unicorns (venture-backed companies with a valuation above USD 1bn) are AI-driven, not bad for a technology that, to public eyes, barely existed three years ago. In more detail, two earlier venture-backed successes, Bytedance (i.e. TikTok) and Uber had been established for 80 months when they launched their first products. OpenAI and Anthropic have done so after 30 months, and each is now worth close to USD 1 trn. Equally, illustrating the link between investor exuberance and AI, the FT recently estimated that two-thirds of the value of SpaceX is attributable to investments made in the company in the six months since December 2025.

When this trio of AI firms lists on the stock market, revised index inclusion rules will add their weight to the already substantial 44% representation of technology stocks in the major indices. To that end, AI is no longer a market theme or fad, but is becoming an asset class in its own right.

One of the factors that distinguishes a genuine asset class from a market theme or fad is the presence of a transformative technology, with a lasting economic impact. In the context of an otherwise pedestrian US economy, AI capital expenditure is the dominant growth driver and in the last year, expenditure on data centres in the US hit USD 1 trillion.

A comprehensive study from Stanford’s Forecasting Research Institute (March 2026) compared GDP forecasts from different types of forecasters – economists in the private sector, academics, AI experts and the general public. Unsurprisingly, those closest to the AI industry tended to have the highest GDP forecasts, while academics were more grounded. On balance though, there is a consensus view that AI will lift the trend rate of growth in the US.

There are also increasingly varied ways to invest in AI. An AI-centric portfolio can now span private equity, venture capital, infrastructure (clean energy for data centres), real estate (data centres), currencies such as the Korean won, corporate bonds (Amazon, Meta, Oracle and Alphabet have issued nearly USD 150bn in bonds this year) and private credit. Indeed, AI-related private credit investments are expected to grow by over USD 1.5 trn in the next two years. While there is already a rich mix of AI-centric asset classes, the correlations between them remain high, limiting the diversification benefit.

In addition to investment banks committing resource to AI-driven deals, another hint that AI is an emerging asset class is that it has its own distinctive mode of corporate governance – strong-willed founders who monopolise voting rights, enormous pay packets and neutered boards. This concentration of control is likely to prove one of the structural vulnerabilities of the AI complex as scrutiny from regulators and institutional investors intensifies.

Given the scale of AI’s footprint across markets, one of the essential tasks for investors will be to identify assets uncorrelated with AI (e.g. luxury goods, food), as well as hedges on AI assets. And, as the suspected AI bubble grows in value, investment managers will have to find ways of protecting portfolios against sharp reversals in AI valuations.

The investment dimension of the AI boom carries particular urgency. Given the risk that AI (as per Mythos) creates potentially existential security and economic risks, and could disrupt labour markets, there is a strategic need for pension funds and sovereign wealth funds to have exposure to the economic benefits of AI. As it stands, the risk is that billions of people will have their lives and livelihoods changed by AI, but the benefits accrue to only a narrow group of investors and executives. In that regard, the advent of AI as an asset class gives individuals, countries and investment funds a means of participating in the upside of the AI boom.

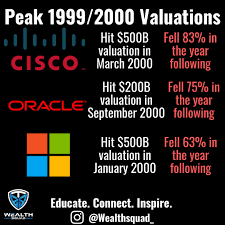

The one formidable obstacle investors will have to navigate is the sense that we are in the thick of an AI bubble. Already long-run valuation measures – such as the ratio of market price to long-run earnings (the ‘Shiller P/E’), or the ratio of the value of the US stock market to GDP – are testing all-time highs, at levels not seen since 1929 and 2000. In this way, AI is truly everywhere, in our savings, investments and pensions, and that will be a risk.

To return to my first point on the switching of analyst roles. A couple of brokerages have, according to the Wall Street Journal’s China correspondent, dropped coverage of Chinese consumer stocks because of the weak outlook for spending. It might be the next trend to watch.

Have a great week ahead, Mike