In 1927, in the context of economic weakness, Benjamin Strong the President of the New York Federal Reserve suggested to a counterpart in the Banque de France that a rate cut might give the stock market a ‘petit coup du whisky’. The subsequent rate cut set in train a fierce market rally which, boosted by margin debt, ballooned into a stock market bubble.

According to Liaquat Ahamed’s superb book ‘Lords of Finance’ Federal Reserve officials had considered the ‘coup de whisky’ to be the Fed’s ‘greatest and boldest operation’. Yet, the collapse of this stock market bubble was one of the factors that set in motion the Great Depression.

By comparison to the actions of today’s Fed, Strong’s ‘coup de whisky’ is insignificant when compared to the huge and sustained quantities of monetary morphine that the central bank has dispensed in recent years. The near vertical rise in central bank balance sheets in the aftermath of the coronavirus crisis has suppressed market volatility, but, like morphine, it cures few underlying economic illnesses. In fact, with the echo of the Great Depression in mind, it may eventually make them worse.

With the Nasdaq index pushing through all-time highs at the start of last week (and now retreating a little), valuations becoming very stretched and an increasingly well documented retail investor trading frenzy occurring, we are entitled to ask where and when the consequences of aggressive central bank activity will lead?

While the official line at the Federal Reserve and other central banks regarding asset price bubbles is that asset bubbles are hard to identify and harder still to burst in a controlled manner, there are at least two risky side-effects of current policy, and then two potential endgames.

The first risk relates to the consequences of the ‘stupefaction’ of the political economy through monetary policy. For instance, politicians, such as the once fiscally conservative Republican party, seem to care less about rising debt and deficit levels in the face of central bank asset purchases.

In Europe, capital markets union, the consolidation and rebuilding of the banking sector, and more active and sophisticated regulation of fintech and payment systems are half made projects that lack urgency. In general, central bankers seem to focus too much on liquidity, than on the plumbing of market and banking systems.

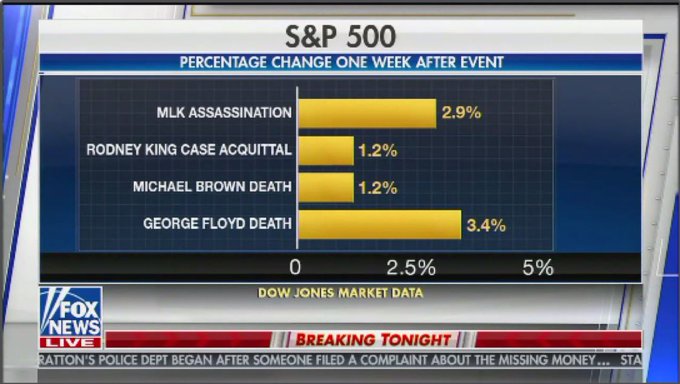

Another side effect is inequality, in multiple forms. Wealth inequality in the US is the most pronounced since before the Great Depression. Another form is central bank inequality. The monetary aggression of the Fed and ECB makes life difficult for other smaller and less activist central banks, through the resulting fluctuations in their currencies for example. In particular in recent years, the likes of the Norges Bank and Riksbank have struggled with the side-effects of ECB policy.

Central bankers are known to be sensible, rational people and in the face of mounting evidence of the distortions of their work and the hint that they are losing their independence, we might expect them to signal an elegantly coordinated end to extraordinary policy. The opposite is likely to be the case.

The great risk to financial stability is that central bankers continue to internalize the benefits of quantitative easing, to the extent that they go into monetary warp factor and break markets. The Bank of Japan, which now owns nearly 80% of the Japanese ETF market, is a candidate here, given the store it sets by monetary activism and discussions it has conducted on monetizing government debt.

Monetizing government debt is not a free lunch, and if for argument’s sake it were executed by the Bank of Japan it could trigger broad currency volatility, a pensions crisis and a very confused credit market. Risk cannot be made to go away, it is simply distributed by markets and central banks that intervene in this process risk a ‘nuclear’ level financial accident.

The second related risk is indebtedness which before the financial crisis was – in terms of the aggregate world debt to GDP ratio – approaching levels not seen since after the Second World War, and now may be on course to reach levels comparable to the aftermath of the Napoleonic Wars. Low rates make this debt load manageable but a credit cycle downturn may result in a market unwind that even the Fed and other central banks cannot forestall. The endgame here may be a severe recession, or an broad debt restructuring conference.

Whether they are ‘Lords of Finance’ or ‘Sorcerer’s Apprentices’ today’s central bankers have contorted the financial world in an effort to stave off another Great Depression, and now having done too much, risk going full circle.

Have a great week ahead,

Mike