We spent a memorable New Year’s Eve on Dursey Island, one of the more remote parts of Europe, whose only point of access to the Irish mainland is by ‘Ireland’s only cable car’, where the principal safety device is a bottle of holy water. In 1602 Dursey was the scene of the massacre of some of the O’Sullivan clan. Some six hundred years before that, it was a staging post for the Vikings.

I am tempted to think that had the Vikings stayed the O’Sullivans could have escaped the slaughter of the Siege of Dunboy, but then again, always optimistic, I contend myself that Dursey – unlike the other Viking island (Greenland) will not attract the attention of the US Navy.

My intention this year is to be as least distracted as possible by the geopolitical strategizing of President Trump, but in the context of a far more ideological cabinet, his thoughts have consequences – not least for how they will encourage the enemies of America and the ‘west’ to behave.

For investors, political and geopolitical risks will likely play a much greater role in developed market asset returns than in any time over the past forty years, and the market reaction to Donald Trump’s victory offers them a wonderful opportunity to take a contrarian view and ‘spend American exceptionalism’.

To explain what I mean by that, our starting point in 2025 is that an array of US assets trade at very high levels. Indeed, to recap a phrase I used in December markets are starting 2025 from the ‘wrong place’ in the sense that an enormous amount of capital is tied up in assets (the top ‘7’ technology firms, the dollar, corporate bonds) that trade at all time lofty valuations.

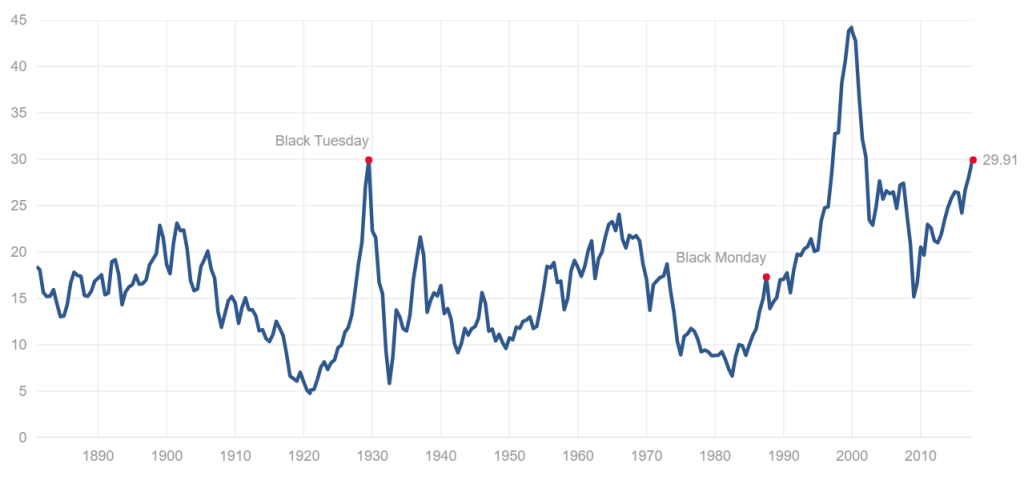

For instance, Bank of America estimates that the dollar is the most expensive that it has been since the early nineties, and valuations for US stocks are close to the highest levels they have reached since the late 1990’s. The top fifteen companies in the US are now worth the same as Chinese and European equity markets together.

Added to that, quite a few assets have exploded in value because of their proximity to Donald Trump – notably the crypto eco-system and Tesla (which has added USD 850bn in market value around the time of the election, an amount equal to the value of its ten nearest competitors).

There is not yet a bubble in the broad US market – many segments such as value stocks (high dividend companies) and small companies have not performed, but there is sufficient capital held in very expensive dollar denominated assets that it demands the attention and action of investors.

Market analysts do not appear worried – in the time-honoured fashion the major investment houses have released their year ahead forecasts, which suspiciously all cluster around the 10% market, and equally suspiciously no investment house is forecasting a negative year for US stocks. This collective conclusion must have required great analytical power because an independent re-running of these same models points to flat or negative returns.

To that end, investors should take advantage of expensive dollar assets and diversify abroad.

They may be convinced to do so by two developments. The first is the collapse in long term US bonds since the Federal Reserve launched into a series of rate cuts from September onwards. In effect the bond market is signaling that it sees a resurgence of inflation ahead, and it is also likely flagging that the credit worthiness of the US may be deteriorating (in the sense that there is little prospect of the budget deficit and government debt being pared back).

Related to this, the second Trump administration begins in a much worse fiscal place as the first Trump government did in 2016. In the period 1960 to 2016 (with the exception of the Vietnam War) the US budget deficit has always followed the tempo of the business cycle (as proxied by unemployment).

That is to say that the budget deficit shrunk when the economy was strong (low unemployment) and it grew when the government spent more to cushion the effects of recession (high unemployment).

Today, we have the opposite – unemployment is low and the budget deficit is very high. This implies three risks – that too much spending in a ‘hot’ economy creates inflation, that there won’t be any money left to ‘rescue’ an eventual recession, and that the rising deficit implies rising debt, which bond markets don’t like.

None of these risks, and rising bond yields, appear to worry the US equity and corporate bond market, but they should. A contrarian view might look to sell expensive dollar denominated assets and allocate overseas.

So my message to start the year is – don’t invade Denmark, buy its equity market.

Have a great week ahead, Mike