When Robert Shiller won the Nobel Prize for Economics in 2013 (shared with Lars Peter Hansen and the great Eugene Fama), I recall being particularly pleased for him. He is, rightly I suspect, a skeptic of the antics of financial markets, having twice called the top in market bubbles (dot.com and housing crisis). He coined the phrase “irrational exuberance,” which was used to powerful effect by Alan Greenspan.

Then, famously during the dot.com crisis, he was derided by many in the financial community and on CNBC for his pronouncements that markets would collapse. He handled himself with grace and had the last laugh. In addition, he is an economist with a practical interest in markets and asset prices, and many of his housing and stock market metrics are now widely used.

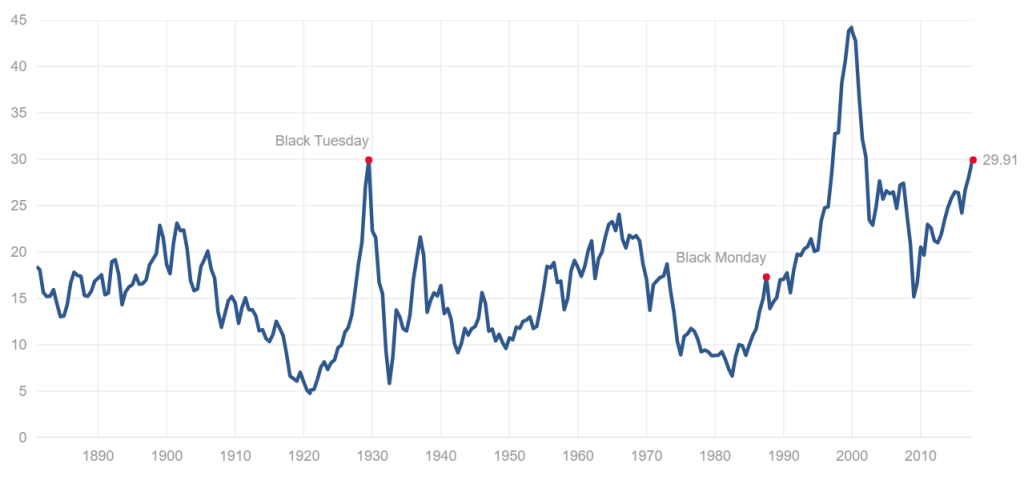

Well before academics shared data publicly, Shiller made his long-term market valuation series available on the internet. This open source approach is perhaps one of the reasons why his long-term data is now widely referred to. The key metric here is what is called the Shiller P/E (price to earnings ratio) or, as he himself puts it, the CAPE, the cyclically adjusted price to earnings ratio. What this essentially does is normalize earnings across the economic cycle.

The CAPE is now at a level only previously reached in 1929 and 1999/2000. We know what happened next in both of those cases. This doesn’t seem to worry investors, largely because the market narrative is built around the notion that ‘a trade deal will be done any day now’ and that the Federal Reserve will continue to dose markets with liquidity.

Interestingly, the idea of the macro ‘narrative’ is the focus of Shiller’s most recent work (he has a book out entitled ‘Narrative Economics’ as well as several papers on the topic). Essentially, he investigates the ways in which we (households, investors, economists) tell stories about the behavior of economic events and market trends. I would argue that ‘The Levelling’ is a narrative on what is happening to the old world order and on how it would evolve.

Shiller’s ‘narrative’ based strand of research is not new. Pop economists have for a long time made sense of the world by coining understandable terms like ‘white van man’, and for an even longer time, stockbrokers have told stories around stocks and markets, and their clients have readily swallowed these stories.

I tend to classify the spectrum of the finance industry as having two ends – storytelling and quant. Story tellers are not good quants, and quants are not good storytellers. What is interesting now is that quant, be it through the provision of new and better datasets, is providing the narrative ammunition for storytellers to tell more elaborate, and possibly convincing, macroeconomic stories.

Storytelling is also a neat way of bunching together the various trends in markets. For instance, there is a notable divergence between what we might call drugged assets (assets that are under the spell of central bank liquidity) such as the Dax, quality corporate bonds, euro-zone debt and the S&P 500 index, and those like emerging market currencies, some commodities and crypto currencies (see last week’s missive) that do not have the outright benefit of central bank asset purchases, and that as a result tell a cleaner picture about the relatively weak global economy.

As we head into December expect many to continue the narrative that central bank liquidity will suppress volatility, and I suspect that in general this narrative will continue to hold into 2020.

One narrative that may pick up pace, is the idea I explored a few weeks ago of ‘Demonstration Contagion’ (link). Under this narrative, the panoply of protests around the world are both distinct and have common perceived causes such as inequality and climate damage. In particular, events in Hong Kong cut across many of these issues, and there is a great deal at stake economically and politically.

The new developments are that President Trump’s (by the way Shiller describes him as a ‘master of narratives’…Shiller is a master of irony) signing of the Hong Kong Human Rights and Democracy Act and the overwhelmingly pro-democracy tenor of last week’s council elections in Hong Kong, provide two threads to tie events in Hong Kong to the trade dispute between the US and China, and to January’s Presidential elections in Taiwan.

As such, protestors in Hong Kong have every incentive to continue to protest, and the Chinese authorities cannot but feel more uncomfortable. As crowds in Hong Kong this weekend hold aloft the image recently tweeted by Donald Trump of his head superimposed on the body of ‘Rocky’, the Demonstration Contagion narrative is only just warming up.

Have a great week ahead,

Mike