On Thursday last, Emmanuel Macron gave his second ‘Sorbonne’ speech (the first was in 2017) which consisted of laying out, once again, his vision for Europe, though in a more bleak way, and as it happens, periodically stating ‘I’ve gone on for too long’, and then speaking for another twenty minutes.

I was in London at the time so didn’t have the opportunity to walk up the hill to eavesdrop on the president, but it did remind me of another Sorbonne speech, given some twelve or so years ago by Jack Lang, in honour of the Irish president Michael D Higgins. Jack Lang was called upon at short notice because Jacques Delors was ill, but he nonetheless gave a very credible talk on Irish culture, notably on the work of the playwright Sean O’Casey.

I left the Sorbonne as soon as the speech finished, and so did Lang and serendipitously I had the opportunity to walk back towards the 4th arrondissement in his company. What I was most struck by was the number of people who stopped Lang in the street, to shake his hand or take a selfie, and I am not sure that there is a French/German or other European politician who would get a similar reaction whilst traipsing across their capital city. The lesson then is that there are votes in culture, but maybe not grand ideas on geopolitics or finance.

To be fair to Macron, he is one of very few European large country leaders capable of setting out a vision for Europe (Stubb and Tusk might also have a go). Some elements of the speech – to make Europe a world leader in spacetech and AI by 2030 are, from my experience, not credible. Similar goals in quantum computing, new forms of energy technology and biotech are.

The real question however, is who is going to pay for it? Is Macron – and Europe for that matter- a Madame Bovary, addicted to fanciful spending with no means to pay for it?

Compared to the US, Europe is much less well equipped to finance these new technologies at scale. Japan and China are also constrained, but China to a large degree can commandeer private industrial capacity.

One early response to the need for Europe to become more dynamic financially was the launching in 2014 of the capital markets union (CMU) which was headlined by the aim of moving corporate financing away from bank lending to deeper capital markets, and the harmonisation of finance regulations so that capital can flow better across the euro-zone.

The capital markets union soon fell by the political wayside (there have been some advances such as the ELTIF – long-term financing product but little has been done to align pension, insolvency and tax frameworks). However, while the likes of Macron are now touting CMU is a necessary part of Europe’s ‘rearming’, EU leaders ducked the chance to accelerate CMU at a summit last week, arguing it would impose greater costs on local asset managers (the reality is that capital markets in those countries – from Ireland to Belgium – continue to shrink).

This is a great disappointment, and it is little surprise then that the overriding tone of Macron’s Sorbonne II speech was urgent. The irony now, given France’s reputation for regulation (the best explainer of this I have read is Augustin Landier and David Thesmar’s ‘Le Grand Méchant Marche) is that it is mostly French officials (Macron, Lagarde, Le Maire) who are pushing for capital markets union. Indeed the former ECB official Christian Noyer has launched a policy initiative in the space.

The sense of urgency should be all the greater when we hear that the US economy (which was the same size as that of Europe before the global financial crisis) is now 70% larger, and that JPMorgan has a market capitalisation as large as the top ten euro-zone banks. America’s ability to fuel innovation and business operations with finance is exceptional, and the failure of governments in many European countries to properly acknowledge this is disappointing.

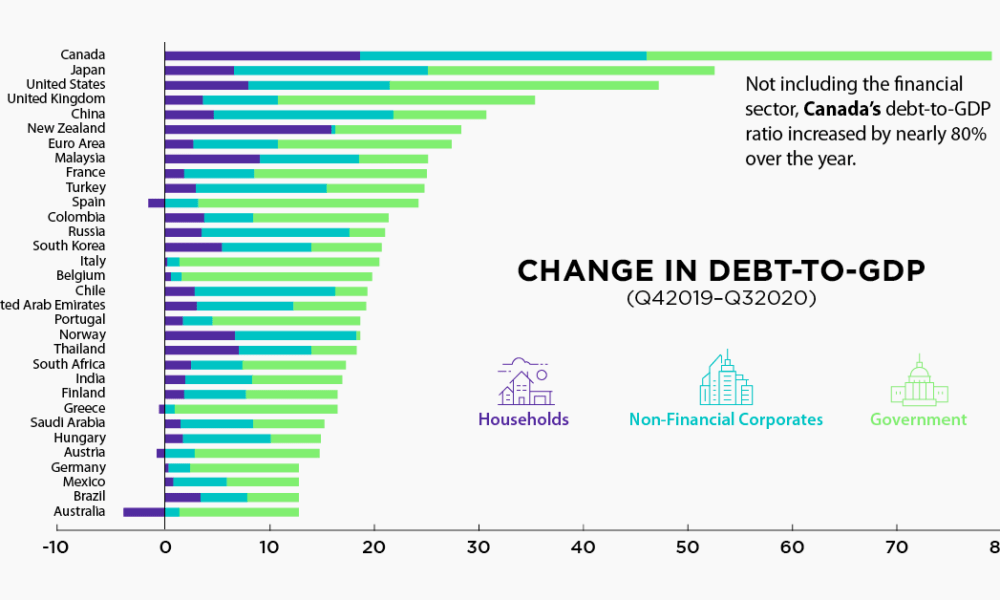

My suspicion is that the paths of least resistance will be the loosening of investment regulations so that wealthier, professional investors can access segments like infrastructure and private equity, and even more likely (this will also be the case in the UK under Labour) that Europe’s technology infrastructure of the future will have to be funded by private capital, much of it from outside Europe. A halfway house towards realising this objective will be to permit state and semi-private pension funds invest more in private equity (along the lines of the Canadian model)

Doing so might also provoke a radical change in governance, where pension funds have to be more active and where there is greater public representation on boards. It is an experiment worth trying, far more so than the option of forcing pension funds to hold more government bonds, and thus saving the political skin of politicians in indebted countries.

Have a great week ahead,

Mike