A recent book, Samuel Moyn’s ‘Gerontocracy in America, highlights the growing concentration of wealth and power in the much older generations in the US, whilst younger generations face historically high valuations in real estate and financial assets, and how this growing intergenerational divide might be mended. Moyn, in my view, has struck a chord that will become one of the new dividing lines in politics, in Asia and the West.

His book brings demographic change into focus, a slow-creeping risk to economies, society and public life, but whose implications are only just surfacing in the public debate. Despite that, from a popular point of view, the sense in many Western countries is that there are too many people, or rather that infrastructure has not kept up pace with population growth – I am writing this in Dublin, which is an excellent case in point.

Yet, the long-run demographic trends – falling fertility, longer life expectancy and a shift in population composition towards a much smaller working (tax paying) population, will have enormous impacts on society, pension systems and debt loads, to name a few economic issues.

As much was evident in Germany’s recent pension reform debate which was nearly upended by Helmut Kohl’s grandson Johannes Volkmann and a group of other young parliamentarians who voiced the right of the younger generation to not have to shoulder the financial burden of their parents’ generation (under the German system, and many others, the working population effectively funds the retirement system of the older generation)..

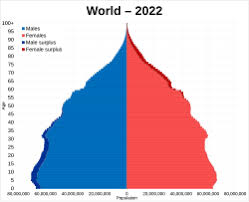

The best starting point on the outlook for demographics is the United Nations World Population Prospects website. and the data – especially in chart form – are quite striking.

The UN data show that as we approach 2100 the world population will plateau and start to shrink. From roughly 2080 onwards the world population growth rate will turn negative for the first time in centuries (wars apart), as the death rate passes out the birth rate. Within the age cohorts, the over 65 group will expand by a billion people in the next thirty years.

More specifically, at the country level, the US death rate will surpass the birth rate in around 2040, and population growth is likely to only be sustained by immigration. The picture is worse for some European countries – Italy for example is already in negative population growth territory, and the most negative forecast scenario from the UN has the Italian population dropping from over 60 million today to 25 million by 2100 (the same level as when Garibaldi unified the country).

Equally, China, which has been renowned for its economic and population growth, will endure a collapse in the 24–65-year age group, who today number 830 million people and by 2100 are expected to comprise 280 million people. China is projected to be the country most affected by ageing, with its, China’s elderly dependency ratio is projected to surpass 100% by 2080, meaning there will be more people aged over 65 than those aged 15 to 65.

The expected collapse in the working population begs serious questions for the economy – who will pay taxes, sustain pension systems and where will demand for financial assets come from. Markets are not worried, yet.

In general, researchers find that there is a positive link between demographics and asset prices, a finding that is predicated on the rise of the boomer middle class and the coincident equity bull market and fall in bond yields. The idea is that until they retire, working households invest more in real estate, equities and other riskier assets, but then shift to income-oriented assets like bonds as they get older and require income from investments. The oddity in that respect is that despite an ageing population, equities and real estate are very expensive. This may well owe to a growing investment culture, a record level of wealth (USD 500 trillion worldwide) and the prosperity boon that has resulted from globalization.

In this context, old money will become a political target, both in terms of demands for lower inheritance taxes, to more populist measures to tax the ‘old’ and give the ‘young’. For governments who worry about demand for their bonds, wealthier older citizens might make ideal candidates for financial repression (their children would face lower inheritance tax provided that capital spent a period of ‘purgatory’ invested in government bonds – I outlined a similar theme in ‘Patriotic Capital’)

At the same time, pension systems will have to change to accommodate a proportionately smaller number of workers (to pensioners). Private pension systems will become more common, they will invest more, earlier, with a tilt to riskier assets.

Concurrently, I expect to hear more on the need for states to establish sovereign wealth like funds (based potentially on the sale of state assets) to help provide for future pension liabilities. Another concern will be the need for states to cushion the potential blow of AI on workforces (a fund that holds equity in AI firms might be an avenue), at least through a transition period. In the long term, AI and robotics may well allow more older people to work for longer and for more women to enter the workforce. And, I haven’t managed to tackle the topic of later retirement ages and how that will impact the workforce and society.

The effects of demographics are not yet showing up in markets, and are just creeping into the investment industry, but it will become a major fiscal and financial megatrend.

It’s that time of year when investors and economists release their prognostics for the year ahead, and eclectic and contrarian as we like to be, The Levelling brings you its top ten themes for 2026, with apologies for the length of the note – in fact this week we are simply giving you the first five themes, with the others to follow next week. It’s really one to print out and read with a coffee, or even a stiff drink.

Given the approach of the holidays, we have also added in some pertinent film and book recommendations.

Some of the ten themes we flag here are based on observations we have made during the year, and relate to trends that are now becoming clearer, chief amongst them is the imprint of AI on economies, geopolitics, and society.

We hesitate to make outright forecasts for GDP and rates for two reasons – first we expect growth to rise modestly during the year (though this is very much dependent on the capex cycle) and second, most of the interesting developments will take place at the sector level.

#1 RAIlway Boom

In the late 1990’s as the dot.com bubble built, there was a polite debate amongst central bankers as to whether or not an asset price bubble was present in stock markets, most notably in dot.com related companies. The upshot of the debate was that even if the central bank could identify a bubble, there wasn’t much it could do to puncture the bubble (notwithstanding Alan Greenspan’s ‘irrational exuberance’ moment).

Today, central banking has changed, and so too have asset bubbles. There is a very broad narrative – from investors and economists – that we are indeed in a ‘bubble’, the only question is whether markets are in the foothills or the peak of the bubble. My sense is more ‘foothills’ than peak, largely because we are not yet seeing the folly and exuberant behaviour that was present in 2000 (I will share some stories in a future note).

Of course, the obvious danger of such a narrative is that for some but not all investors, it permits the belief that investors can continue to buy very expensive assets and later hand them off to ‘greater fools’, and the illusion that ultimately they are not the fools.

Every asset bubble needs an underlying logic, a belief that ‘this time its different’ and this is supplied in spades by the adoption and investment in Artificial Intelligence (AI). Signs that companies and households are deploying AI are manifold. This bubble is also different in the case that AI is producing revenues, as evidenced in the operating and market performance of large AI centric firms (the so called ‘Magnificent Seven’ companies who together now make up nearly 40% of the US stock market capitalization), but those earnings are predicated on the success of the AI business model and are increasingly circular, in that investment by META becomes revenue for Nvidia and so on.

What is altogether less clear to me is how the economics of AI play out. While the adoption of AI is occurring more quickly than other technologies (the internet), competition will surely lower margins quickly. Chinese projects are a case in point, and some of the large US AI platforms, of which OpenAI is the leader, may find their economic models undercut.

Neither is the distribution of the productivity benefits that convincing – specialized firms and operators with access to proprietary data will be able to leverage AI to great benefit, along the lines of my ‘One Man and his Dog’ thesis. However, for most people, once some basic administrative tasks have been swallowed by AI applications, the positive economic impact on their lives might be more limited. Another consideration is that AI model technology is in the hands of a small number of investors, so the capital productivity benefits of it can also be limited.

The Future:The AI boom or bubble is gathering momentum. Levels of capital investment (relative to GDP) are already surpassing those of prior bubbles, but have not yet attained the giddy heights reached during the railway bubble of the 1900’s. The railway bubble was one of the great asset bubbles – and helped build the crucial infrastructure of the first wave of globalization. In 1900, investment in railway infrastructure amounted to 6% of GDP, AI today is just over 1.3%. Also, at the turn of the 19th century nearly 60% of the market capitalization of the US stock market was made up of railway stocks (today it is 0.3%) which as a rule of thumb suggests we might see talk of a USD 10 trn valuation for Nvidia and SPX 10,000 ((the US S&P500 index hitting 10,000 points) as a ‘sell everything’ moment.

Read:Charles Kindleberger’s ‘Mania’s, Panics and Crashes’

#2 ‘Dalloway’

One of the more memorable films I saw in 2025 is Dalloway, a French film starring the ever-excellent Cecile de France, which I hope will make its way to the Anglophone world. The object of the film is to show how pervasive and sometimes pernicious AI could become as a social force, and as we head into 2026, this is a theme that will become more important – in healthcare, labour markets and society – and more startlingly obvious.

To start with an alarming example, in 2021 the Swiss government’s Spiez Laboratory, one of whose specialisations is the study of deadly toxins and infectious diseases, is located right in the heart of Switzerland, performed an experiment where they deployed their artificial intelligence driven drug discovery platform called MegaSyn to investigate how it might perform if it were untethered from its usual parameters.

Like many AI platforms MegaSyn relies on a large database (in this case public databases of molecular structures and related bioactivity data) which it ordinarily uses to learn how to fasten together new molecular combinations to accelerate drug discovery. The rationale is that MegaSyn can avoid toxicity. In the Spiez experiment MegaSyn was left unconstrained by the need to produce good outcomes, and having run overnight, produced nearly 40,000 designs of potentially lethal bioweapon standard combinations (some as deadly as VX). It is an excellent example of machines, unconstrained by morality, producing very negative outcomes. It’s a chilling tale of the tail risks of AI.

More commonly, AI will increasingly become part of our economic and social lives, and its effects will be more apparent.

In labour markets, there is already plenty of evidence to suggest that AI is curtailing hiring, markedly so in the case of graduates. When AI and robotics start to combine, they can have very positive outcomes (in education and elderly care) but in warfare (see the Netflix documentary ‘Unknown Killer Robots’), fruit picking, warehouse management and even construction – to give a few examples, the blue collar labour force will feel the effect. This could set up a political reaction, and we might well see a Truth Social post from the White House to the effect that AI is not such a great idea and needs to be regulated.

A potential side-effect of the more negative effects of AI on the labour market could be a rise in anxiety and what social scientists call ‘anomie’. Much the same is becoming clear from the ways in which social media is skewing the sociability of humans (think of declining fertility rates, pub closures and the mental health effects of social media). As such, the social effects of AI may lead to ‘deaths of despair’. If this is grim, there is potentially very positive news in the use of AI to improve medical diagnoses in inexpensive ways, and the marginal impact of this in emerging countries can potentially be very significant (leading AI firm Anthropic is targeting science and healthcare in terms of applied AI solutions).

The Future:The economic and social side-effects of AI will become clearer – many of them will be positive, but others will start to provoke a political reaction. While the EU has softened some of the restrictions in the EU AI Act, the interesting development is that at the state level in the US there is a growing desire to curb some of the effects of AI, a trend that is supported by case law. Moreover, local politicians in the US (Republican Josh Hawley is an example) are more vocal about the negative side-effects of AI on labour markets and education.

Read:Carl Benedikt Frey ‘The technology Trap’(2019), and Robert Harris’ ‘The Fear Index’ (2011)

Watch: ‘Dalloway’ (1997)

#3 AI Cold War

A further facet of AI to keep an eye on is geopolitics, and as we leave 2025 behind, we will hear more about the notion of an AI Cold War or ‘Sovereign AI’ according to a good Pitchbook note. This emerging idea refers to the strategic uses of AI, in the context of strategic competition between the ‘great’ powers. This race is already on, and the US is in the lead, with China chasing behind (my recent note on The Plenum details how China is prioritizing frontier technologies as the spearhead of its economic plan). Europe is very much in third place, with energy policy and half formed capital markets the biggest obstacle.

In a ‘Cold War’ AI world, model development and deployment increasingly take a multipolar form (see #8 below), regulation is competitive and technology firms closely align with governments – forming symbiotic parts of national infrastructure – while national security considerations are embedded into investment processes and supply chain planning. In time, governments may steer model developers towards new datasets if there is a strategic advantage to be gained.

The Future:From an investment point of view, we expect private equity/credit to become an enabler of this trend, and for their part governments will open up the flow of pension capital to private asset classes. Governments may also become more active investors – either in steering merger and consolidation activity, or in the fashion of the Trump administration, taking stakes in firms that are judged to be strategic. Military uses of AI will become more commonplace, and we will slowly learn more about the effects of this on navigation systems, genetics, finance and social media, to name a few.

Read: ‘Breakneck’, by Dan Wang (2025), ‘Chip Wars’ by Chris Miller (2022)

Watch: Dr Strangelove (1964)

#4 Expensives to Defensives

An age-old joke goes that when asking for directions, the traveller is told ‘I wouldn’t start from here’. It is much the same for investors looking into 2026, though less so tactical traders who believe that they can time the ebbs and flows of the emerging stock market bubble.

The dilemma for asset allocators is that with the US stock market making up some 60% plus (depending on the benchmark) of world market capitalization, and trading at near record valuation multiples (price to earnings or price to long term earnings (Shiller PE), or even market capitalization to GDP (Buffet Indicator), the exposure to American assets is increasingly expensive and risky.

For example, a model that combines monetary, business cycle and market valuation indicators, suggests that from this point onwards, returns in the next couple of years for US equities will be close to zero. Add to that the fact that the dollar still looks expensive and corporate bond (and high yield) spreads are very narrow, and the conundrum for allocators next year will be considerable.

As we end the year, volumes have been very low and speculative activity (options) very high, and this points to high levels of volatility through 2026, and remarkably, a few of the large bank CEOs have warned of significant market drawdowns.

The Future:We expect to see investors put more money to work in cheaper defensive sectors – Staples and Healthcare for example, and for capital to flow to other regions beyond the US. In addition, in the next five years, if multiple surveys of family offices and pensions are to be taken at face value, we expect private assets to make up a much more significant proportion of investment portfolios.

Read: Benjamin Graham ‘The intelligent Investor’ (1949)

Watch: ‘Margin Call’(2011), ‘The Big Short’(2015)

#5 K Shaped economy

In the context of a political-economic climate in the US where good, regular economic data is hard to come by, commentary from industry leaders as they report earnings is providing some fascinating insights. For example, some weeks ago, Chipotle, the burrito chain, reported a surprise drop in revenues because two key consumer groups, households earning USD 100k or less, and younger customers (24-35 years old) are cutting back discretionary spending, even on fast food.

A range of firms with similar client bases underline this trend – car manufacturers report that sales of expensive, large vehicles are strong, but that lower income customers are preferring smaller, fuel-efficient models. McDonalds is revising its ‘extra value meal’ option, and credit card providers like Amex report very different types of activity from rising card balances and distress in the lower segments, to robust spending in its ‘Platinum’ category.

Economists are blithely referring to this phenomenon as the ‘K-shaped’ economy, whistling past the graveyard of economic history that portends revolutions are made of such obvious divergences in fortune.

Now all of the talk is of a K shaped economy – which refers to multiple divergences between the price insensitive wealthy and those in economic precarity who are sensitive to inflation, a services sector that is either shedding jobs and holding back from hiring compared to the upper echelons of the technology and finance industries where unprecedented levels of wealth are being created.

There are two other effects ongoing. The first is the economic effect of AI-focused capital expenditure (across the energy, logistics and technology sectors). The second, more important trend is a mangling of business cycles, such that few of them are synchronized across geographies, or between the real and financial economies (German chemicals is in the doldrums but German finance is on an upswing).

Yet, a better diagnosis might be the ‘Marxist’ economy – one where the owners of capital and the source of labour are at odds.

The Future:In the US, the top 10% of the population own 87% of stocks and 84% of private businesses, according to data from the Federal Reserve. On the other hand, we have previously written about the rise of economic precarity in The Road to Serfdom. So, whilst it is a new observation amongst the commentariat, the diverging fortunes of capital and labour should start to trouble policymakers in 2026. Expect this to be a headline policy issue net year – the White House is already paring back some tariffs, and in Europe governments compete to either tax the wealthy (France and the UK) or to lure them (Italy).

One of the favourite books I have received as a gift is ‘Bushido’, the framework of the Japanese code of chivalry. I was given the book in the very early 2000’s, when it was not yet obvious that Japan would stagnate for quite so long and, the talk was still of the collapse in Japanese golf club membership prices

Indeed, one of the remarkable socio-economic trends in Japan up to the mid-1990’s was the startling rise in Japanese gold club membership fees, which in the heady 1980’s Japan, had become a tradeable asset, so much so that an index was created (always a warning sign). During the period 1982-1989 the average golf club membership fee rose by 400%, with a final 190% spurt from 1989 to 1990. Companies such as Ginza Golf Services initially made a lot of money trading golf club memberships and at the peak of the market some were changing hands for close to USD 3mn.

Naturally, this bubble collapsed, and as a nod to the future I flag a blogpost from ‘GolfProp’ magazine that shows that on average entry fees for American gold club memberships have been increasing at a rate of 23% per annum since 2019. Indeed, within the past year the membership fee at Mar-a-Lago has gone up by 43%

Back to Bushido, which as a noble, chivalric code developed in the 16th century, is unlike European ‘Chivalry’ (see Maurice Keen’s book of this title is a must read) in that the idea of ‘Chivalry’ came about much earlier, and largely because of an effort to stop the knights of Europe killing each other in jousts and disputes. Bushido is still part of the mindset of many Japanese, and Japan is increasingly unique as a country where very strong social codes frame behaviour.

To that end, the sense of bushido and Japanese diplomacy will have been taken aback by the unexpected decision by President Trump’s to slap a 25% tariff on America’s main allies in Asia, Japan and South Korea. Japan has always enjoyed close ties to the US (Al Alletzhauser’s 1990 book ‘House of Nomura’ is a very good account of how America helped build the modern Japanese financial and corporate system). I have a sense that another book of that era, Ezra Vogel’s ‘Japan as Number One’, seems to have stuck in Trump’s mind (in the 1990’s he went on CNN to castigate Japan American foreign and trade policy on Japan).

Trump and ‘bushido’ are anathema to each other, and the Japanese will be disappointed by his behaviour, given that Tokyo has always had close relationships with American presidents – though never as close as that with Jacques Chirac who visited Japan over 40 times (for various reasons which I shall not disclose).

The potential rupture in relations between Tokyo and Washington introduces a strategic dilemma for Japan, at a time when its economy is awakening from decades of slumber. Like the UK, Japan’s geopolitical moorings are coming unstuck. President Macron’s state visit to London shows the direction of travel for the UK on security and defence, and whilst it is accelerating defence spending, Japan may end up considering more radical solutions for its defence in the context of Chinese belligerence (in 2024 Japan’s air force scrambled jets 704 times against incursions by Chinese and Russian jets). For instance, Japan is the one country that could quickly build a nuclear weapons programme, if it needed to.

What is interesting in the Japanese case is that as geopolitical uncertainty rises, its economy and financial markets are thawing. The property sector is just reaching levels last seen in the early 1990’s (while Tokyo prices have recovered beyond 1991 levels, the rest of the Japan’s residential market is still below the price point reached then).

Having suppressed bonds yields for a long time, the Bank of Japan is now raising rates, and Japanese bond yields have been pushing higher, and given the size of the Japanese bond market (and the balance sheet of the Bank of Japan), it is driving yields higher internationally, and deserves watching as a medium-term risk to markets.

However, while bond yields are rising in the absence of yield curve control by the central bank, factors that are regarded as engines of the economy – earnings, consumer behaviour and employment are more muted, and give rise to the sense that Japan is either in the ante chamber of a full recovery, or on the precipice of something nastier.

Tariffs, and a confusing break with the US, could upset the Shigeru Ishiba’s unpopular government (Upper House elections are soon), which is struggling in the context of a very ‘un-bushido’ world.

We spent a memorable New Year’s Eve on Dursey Island, one of the more remote parts of Europe, whose only point of access to the Irish mainland is by ‘Ireland’s only cable car’, where the principal safety device is a bottle of holy water. In 1602 Dursey was the scene of the massacre of some of the O’Sullivan clan. Some six hundred years before that, it was a staging post for the Vikings.

I am tempted to think that had the Vikings stayed the O’Sullivans could have escaped the slaughter of the Siege of Dunboy, but then again, always optimistic, I contend myself that Dursey – unlike the other Viking island (Greenland) will not attract the attention of the US Navy.

My intention this year is to be as least distracted as possible by the geopolitical strategizing of President Trump, but in the context of a far more ideological cabinet, his thoughts have consequences – not least for how they will encourage the enemies of America and the ‘west’ to behave.

For investors, political and geopolitical risks will likely play a much greater role in developed market asset returns than in any time over the past forty years, and the market reaction to Donald Trump’s victory offers them a wonderful opportunity to take a contrarian view and ‘spend American exceptionalism’.

To explain what I mean by that, our starting point in 2025 is that an array of US assets trade at very high levels. Indeed, to recap a phrase I used in December markets are starting 2025 from the ‘wrong place’ in the sense that an enormous amount of capital is tied up in assets (the top ‘7’ technology firms, the dollar, corporate bonds) that trade at all time lofty valuations.

For instance, Bank of America estimates that the dollar is the most expensive that it has been since the early nineties, and valuations for US stocks are close to the highest levels they have reached since the late 1990’s. The top fifteen companies in the US are now worth the same as Chinese and European equity markets together.

Added to that, quite a few assets have exploded in value because of their proximity to Donald Trump – notably the crypto eco-system and Tesla (which has added USD 850bn in market value around the time of the election, an amount equal to the value of its ten nearest competitors).

There is not yet a bubble in the broad US market – many segments such as value stocks (high dividend companies) and small companies have not performed, but there is sufficient capital held in very expensive dollar denominated assets that it demands the attention and action of investors.

Market analysts do not appear worried – in the time-honoured fashion the major investment houses have released their year ahead forecasts, which suspiciously all cluster around the 10% market, and equally suspiciously no investment house is forecasting a negative year for US stocks. This collective conclusion must have required great analytical power because an independent re-running of these same models points to flat or negative returns.

To that end, investors should take advantage of expensive dollar assets and diversify abroad.

They may be convinced to do so by two developments. The first is the collapse in long term US bonds since the Federal Reserve launched into a series of rate cuts from September onwards. In effect the bond market is signaling that it sees a resurgence of inflation ahead, and it is also likely flagging that the credit worthiness of the US may be deteriorating (in the sense that there is little prospect of the budget deficit and government debt being pared back).

Related to this, the second Trump administration begins in a much worse fiscal place as the first Trump government did in 2016. In the period 1960 to 2016 (with the exception of the Vietnam War) the US budget deficit has always followed the tempo of the business cycle (as proxied by unemployment).

That is to say that the budget deficit shrunk when the economy was strong (low unemployment) and it grew when the government spent more to cushion the effects of recession (high unemployment).

Today, we have the opposite – unemployment is low and the budget deficit is very high. This implies three risks – that too much spending in a ‘hot’ economy creates inflation, that there won’t be any money left to ‘rescue’ an eventual recession, and that the rising deficit implies rising debt, which bond markets don’t like.

None of these risks, and rising bond yields, appear to worry the US equity and corporate bond market, but they should. A contrarian view might look to sell expensive dollar denominated assets and allocate overseas.

So my message to start the year is – don’t invade Denmark, buy its equity market.

Winter it seems, across much of Europe, has come early. Two instincts that grow as the evenings darken are the inclination to have a tipple in the evening and to watch a good film. One Danish work that captures both sentiments is ‘Druk’ or ‘Another Round’, which won the Oscar for best international film in 2021. I recommend it.

In the film a group of four school teacher friends decide to test the hypothesis of a Norwegian psychologist that humans have a deficiency of alcohol in their blood, and the protagonists undertake an experiment to maintain a ‘warm’ level of alcohol in their blood. It is an experiment I attempt often, but the real lesson today is with central banking.

It seems that central bankers have decided that in the spirit of ‘Druk’, the liquidity in the world financial system is not sufficient and have set out to administer near daily injections of cheap money. The number of central banks changing policy (i.e. to negative) is the greatest it has been, apart from the global financial crisis and the COVID period. In September alone there have been 24 rate cuts from central banks around the world.

Chief amongst these has been the 50-basis point cut from the Federal Reserve and the very dramatic, multiple policy moves by China. In short China has cut rates, infused the banking system, made mortgages cheaper and generally tried to spread liquidity over the emerging cracks in China’s economy. In the spirit of ‘Druk’ it is the equivalent of going on a five day bender in order to cure a serious disease.

Nonetheless, the easing in policy from the Fed and China, together with what will likely be a couple of more rate cuts this year from the European Central Bank mean that the world financial system is flush with liquidity. Chinese markets – hitherto the worst performing markets of a major economy – show the impact and importance of liquidity. The market cap of the Hang Seng index has grown by a quarter in less than two weeks. China has overtaken the US in terms of equity market performance to date.

There is no change to fundamentals – I don’t see this policy move having a decisive impact on the downward trend in Chinese earnings, but that doesn’t matter in the near term – liquidity is coursing through the pipes of the Chinese financial system, and in turn might bring a temporary easing to conditions in the property market.

For all the analysts who devote time to measuring earnings and calibrating valuations, the reality is that in this era of ‘quick to please’ monetary policy, liquidity matters a lot for asset prices. My rule of thumb in constructing a measure of liquidity would encompass money supply, the state of central bank balance sheets, the key role of the dollar and net issuance of debt by treasuries.

The arcane notion of financial liquidity has attracted enough attention that the Financial Times recently ran an article breaking down its component parts. A couple of top-flight economics consultancies run their own measures of liquidity – such as LongView Economics and Michael Howell at CrossBorder Capital. The latter holds that we are on the cusp of a significant upswing in global liquidity.

If that is true, the implication for markets is ‘Druk’- a persistent giddyiness whilst central banks keep rates low and liquidity flush, amidst an acceptable level of GDP and profit growth. Friday’s job market figures in the US were very strong, suggesting that in fact there was no need for a large rate cut. This is the kind of macro climate we have seen in the mid and late 1990’s, and one that tends to dampen the market implications of turbulent geopolitics.

From the point of view of asset prices, there are a couple of possible trajectories. Historically, the Fed has started to cut interest rates when the price to earnings ratio on the S&P 500 has been close to 10 times (1960’s to 1990’s). Now, like in 2000, it is in the mid 20’s which suggests that extra liquidity now could run asset prices in bubble territory proper, and cultivate the next bout of inflation, something the central banks’ bank, the BIS, has warned about (helpfully the BIS has taken a counter view to that of its members ahead of a number of crisis).

For the time being, the upturn in liquidity may be most meaningful for capital markets activity and assets in the private economy. They have been in the doldrums. If the ‘Druk’ hypothesis is working we should see a rise in IPO activity into 2025, and intensification in private equity deals and a rise in funding activity (beyond AI firms) in venture.

I started the week chatting with one of the leading experts on globalisation, or deglobalization’ as it is now. He is a little older than me (he won’t mind me saying) but we share much the same formative experiences, notably an internalising of the way the world worked in the 1990’s and 2000’s.

Back then, the big project was the construction of the euro, to the chorus of debates on global imbalances, fiscal strength (Hans Tietmeyer the former Bundesbank chief would be horrified by Western economic policy today). Elsewhere in the late 1990’s forward guidance of monetary policy consisted of analysing the size of Alan Greenspan’s briefcase and there was a healthy debate on whether central banks should act to burst asset bubbles (today central banks seem to trade those bubbles).

The point of this reminiscence is twofold.

The first is to demonstrate that compared to previous decades (and indeed the long-run of economic history) today’s economic landscape is an aberration, out of kilter with most long-term expectations of how economies behave.

The second point is to illustrate that for very long periods, economies follow regimes of behaviour where very different norms can endure for some time. It is often the correction of these norms that triggers large scale shifts in asset allocation, and volatility. One marked echo of market behaviour today, with the early 2000’s is that the equity risk premium (the benefit of owning equities over bonds) has fallen to its lowest level since 2000, and the performance of smaller companies (to very large ones) is the weakest it has been since 2001.

In general, the 1990’s and 2000’s were periods of rising expectations, whereas today that is not generally the case across countries. A notable feature of the sense that ‘things were on the up’ in the 1990’s was the growth of emerging markets.

Indeed, that period has given us at least two economic miracles – the rise of China as an economic and geostrategic power, and the rise of small, emerging states (Singapore and the Emirates). Neither of these ‘miracles’ is given enough credit by the West for what they have done in such a short space of time.

Specifically, last week was highly instructive in the case of emerging economies – three elections registered high market volatility. Mexico has elected a new president amidst fears that the institutions of the state, and its democracy will be further undermined, combined with a leftward tack on economic policy. The peso reacted badly.

India surprised most commentators (the consensus view on Modi has been far too bullish) by failing to ‘ordain’ Modi’s third term in office with a wholesome majority. While this may be positive from the point of view of India’s democracy, it means that the Modi economic steamroller has less momentum.

Then, the failure of the ANC to regain their majority in South Africa should not be a surprise given the failure of that economy to grow much in the last fifteen years (GDP per capita is at the same level as it was in 2010).

In the cases of India and Mexico, markets appear to be pricing democracy very differently – less of it in Mexico is bad, but the checking of Modi’s near absolute power is also bad (at least for the notion that he could have forced through another round of government spending).

Similar to governments across many emerging countries, investors appear to be torn between the strong man model and the Western oriented rule of law one. This is just one parameter where emerging economy governments will be forced to choose – another is between the US and China, and a further one is how to build an economy (and cities) around new technologies and in a more efficient way.

Of the three countries, South Africa is a depressing warning to others, and I see very little hope that it can put in place a coherent developmental model. What is more reassuring is that there are plenty of examples of countries that have made the journey from emerging markets to stable economies – Poland, the Czech Republic and the Baltic states are good examples, and the cohort of Vietnam, Indonesia, Thailand and Malaysia is on its way. Other emerging economies like Nigeria and Argentina are ‘experimental’.

What is also interesting is that emerging markets show that investors are becoming more sensitive to political and institutional risks (institutional investors in Turkey have all but given up). In this respect the important question is whether they start to more severely price in the macro risks associated with some of the developed economies.

If my notional 1990/2000’s investor was to return to the marketplace today, he/she would be confounded by valuations, low volatility and miniscule credit risk, and might start to believe that markets should treat the developed world economies with the same mercilessness it has shown to emerging markets this week.

John Maynard Keynes is very well known for his contributions to economics and policy making, but less so for his investing prowess. In the 1920’s Keynes worked as a portfolio manager for two insurance companies and from 1921 to 1946 ran the endowment (the ‘Chest’) for King’s College, Cambridge. Keynes’ investing performance is the subject of some fascinating research by David Chambers and Elroy Dimson.

Early in his career Keynes was what we might call a macro investor, focusing on commodities and foreign exchange. Later, he became more focused on stocks, and from the 1930’s Keynes beat the (stock) market by over 5% per year despite several close shaves with personal bankruptcy.

Viewed from the point of view of today’s stock market, what was unusual about Keynes’ style was that in the 1920’s and 1930’s equities were very much the preserve of retail investors, and not so much institutional managers.

To that end, Chambers and Dimson remark that Keynes’ early allocation to equities was ‘as radical as the much later move to illiquid assets in the late 20th century by Yale’. Unsurprisingly, Keynes’ investing style, which was driven by strong macro-economic views and focused on a few, large and often concentrated positions (if he was investing today he would likely be heavily invested in mega-cap technology stocks) has influenced modern endowment managers, most notably David Swensen of Yale.

Swensen pioneered the move by large US university endowments towards private assets (notably private equity, but also infrastructure and venture), a strategy that has proven remarkably profitable. The top endowments, generally Ivy League schools and other top ranking universities like MIT, have consistently made double digit returns, spurred by annual §private equity returns in the very high teens.

However, the endowment model is coming under scrutiny, partly because some universities have overinvested in private assets at a time when capital distributions have slowed (my former employer Princeton University has effectively invested up to 40% of its portfolio in private equity and venture), and partly because universities themselves have adjusted their expenditure upwards whilst they have enjoyed generous disbursements from performing endowments.

Endowments in the US originally paid 4% of their value to universities annually but in some cases this has risen to 12% (in turn pressuring endowment managers to produce returns). Broadly, disbursements from endowments amount to close to 30% of university budgets with much of it spent on student financial aid. Given that cash distributions from private equity funds have slowed, the knock on to university spending is being felt.

Anyone who has visited a top-flight US university and witnessed the extent to which laboratories, sports facilities and student bursaries are well funded will appreciate the size of university budgets and the role that endowments play. In Europe, only ETH Zurich can match this level of financial backing.

The debate on endowment investing has been enlivened by the publication in February of the 50th NACUBO Endowment Study. In general, the nearly 700 endowments surveyed in the report hold less fixed income than I would imagine for a typical ‘balanced’ investor, more ‘foreign’ equities than US (this might explain some underperformance), and nearly 50% alternative assets (including a large slug of hedge funds).

Interestingly from the point of Keynes’ active management stance, nearly 50% of US endowments ‘outsourced’ their investment office function. Reflecting this, allocations to private equity, returns and return distribution tend to be better in the larger endowments that have well-equipped investment teams.

In turn this reflects the reality that private equity and venture are two of the asset classes (unlike equity and bond funds) where returns are highly dispersed (i.e. there is a large difference between the best and worst performing funds). As such, finding the best performing funds and gaining access to them has a cost in terms of investment research resources. To this end, I wonder if many universities have really been following the ‘endowment’ model as pioneered by Keynes and Swensen.

Indeed, one of the secrets of the performance of the Yale and Harvard models is that they have very good networks of alumni in the private investment industry, who willingly proffered the best advice and access to their alma mater.

Supporting this theory, Keynes had a similar network of former students around the world (notably in Africa – think mining stocks and commodities) who offered him advice, information and investment opportunities and he also had access to relatively sophisticated telegram technology, so that in some cases he had access to market moving information before others. Further, Keynes was unlike many investors today in that his colleagues at King’s had great faith in him and gave him enormous freedom to pursue his own investment style.

This ‘freedom’ has been all but quashed by benchmarking and technology in public markets (i.e. equity and bond funds) but still exits in private markets – the trick is to find the Keynes like managers.